Description

Random Walk Index technical indicator was originally developed by Michael Poulos.

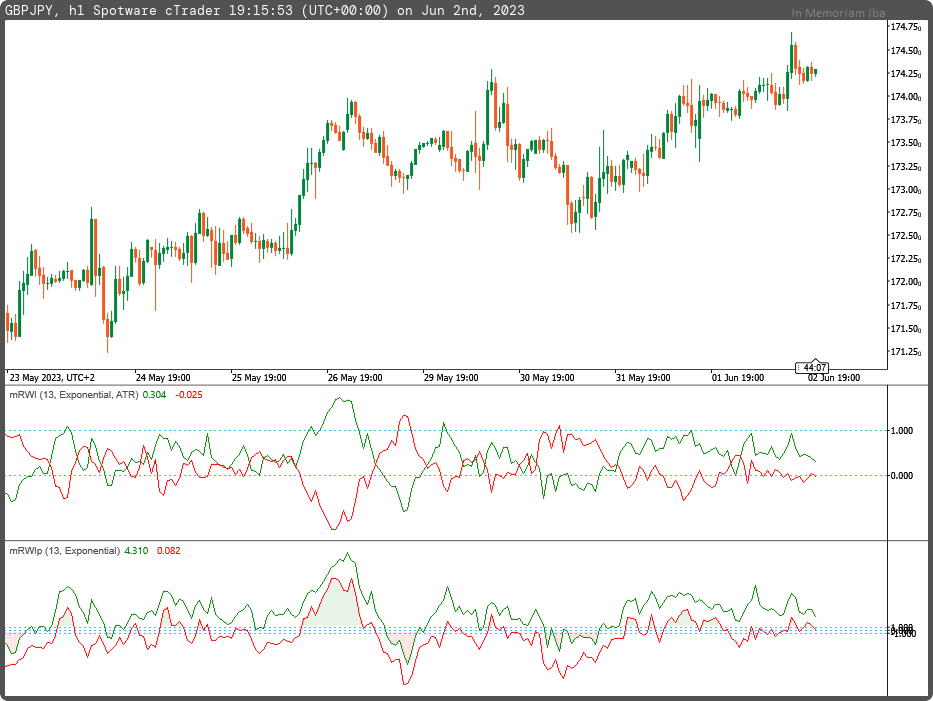

The RWI compares a security's price movements to random movements in an effort to determine if it's in a statistically significant trend. It can be used to generate decisive signals based on the strength of the underlying price trend.

In this original version, the levels 0 and 1 are considered as logical trigger values. Additionally, the calculation method is generated using ATR or Range methods.

using System;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo

{

[Levels(0)]

[Indicator(IsOverlay = false, AutoRescale = true, AccessRights = AccessRights.None)]

public class mRWI : Indicator

{

[Parameter("Period (13)", DefaultValue = 13, MinValue = 2)]

public int inpPeriod { get; set; }

[Parameter("ATR SmoothType (ema)", DefaultValue = MovingAverageType.Exponential)]

public MovingAverageType inpSmoothType { get; set; }

[Parameter("Result Type (atr)", DefaultValue = enumResultTypes.ATR)]

public enumResultTypes inpResultType { get; set; }

[Output("RWI Bulls", LineColor = "Green", PlotType = PlotType.Line, LineStyle = LineStyle.Solid, Thickness = 1)]

public IndicatorDataSeries outBulls { get; set; }

[Output("RWI Bears", LineColor = "Red", PlotType = PlotType.Line, LineStyle = LineStyle.Solid, Thickness = 1)]

public IndicatorDataSeries outBears { get; set; }

private AverageTrueRange _atr;

private IndicatorDataSeries _range, _rwibulls, _rwibears;

protected override void Initialize()

{

_atr = Indicators.AverageTrueRange(inpPeriod, inpSmoothType);

_range = CreateDataSeries();

_rwibulls = CreateDataSeries();

_rwibears = CreateDataSeries();

}

public override void Calculate(int i)

{

_range[i] = Bars.HighPrices[i] - Bars.LowPrices[i];

_rwibulls[i] = (Bars.HighPrices[i] - (i>inpPeriod ? Bars.LowPrices[i-inpPeriod] : Bars.LowPrices[i])) / ((inpResultType == enumResultTypes.ATR ? _atr.Result[i] : _range[i]) * Math.Sqrt(inpPeriod));

_rwibears[i] = ((i>inpPeriod ? Bars.HighPrices[i-inpPeriod] : Bars.LowPrices[i]) - Bars.LowPrices[i]) / ((inpResultType == enumResultTypes.ATR ? _atr.Result[i] : _range[i]) * Math.Sqrt(inpPeriod));

outBulls[i] = _rwibulls[i];

outBears[i] = _rwibears[i];

}

}

public enum enumResultTypes

{

ATR,

Range

}

}

mfejza

Joined on 25.01.2022

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: mRWI.algo

- Rating: 0

- Installs: 351

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

No comments found.