Topics

Replies

afhacker

27 Sep 2018, 13:40

It's possible to get TradingView alerts data and use it as a trading signal on your cTrader trading account, you can do it directly from cTrader Automate API or by using Spotware Connect API.

Post a job request in the Jobs page and somebody will develop it for you,

@afhacker

afhacker

26 Sep 2018, 17:03

( Updated at: 21 Dec 2023, 09:20 )

RE: RE:

andresfborrero97@gmail.com said:

ColossusFX said:

Have you guys seen this?

cMulti

Copy trades to & from multiple cTrader accounts.

cMulti - Copy trades to & from multiple cTrader accounts.

I have been using this to manage accounts for friends.

You set which account/s you want to copy from and all trades are copied in real time.

Yeah, although it looks like a nice tool... It lacks scalability for enterprise use... It says it is a PAMM when it really is just a personal mirror assistant for copying trades.

Thanks still

Where did it say its a PAMM? cMulti (cMAM) is a tool for managing multiple cTrader accounts.

@afhacker

afhacker

21 Sep 2018, 07:21

For double generic collections you can use this method:

public static double Correlation(IEnumerable<double> x, IEnumerable<double> y)

{

double xSum = x.Sum();

double ySum = y.Sum();

double xSumSquared = Math.Pow(xSum, 2);

double ySumSquared = Math.Pow(ySum, 2);

double xSquaredSum = x.Select(value => Math.Pow(value, 2)).Sum();

double ySquaredSum = y.Select(value => Math.Pow(value, 2)).Sum();

double xAndyProductSum = x.Zip(y, (value1, value2) => value1 * value2).Sum();

double n = x.Count();

return ((n * xAndyProductSum) - (xSum * ySum)) / Math.Sqrt(((n * xSquaredSum) - xSumSquared) * ((n * ySquaredSum) - ySumSquared));

}

@afhacker

afhacker

21 Sep 2018, 07:16

public static double GetCorrelation(DataSeries dataSeries, DataSeries otherDataSeries)

{

double[] values1 = new double[dataSeries.Count];

double[] values2 = new double[dataSeries.Count];

for (int i = 0; i < dataSeries.Count; i++)

{

values1[i] = dataSeries.Last(i);

values2[i] = otherDataSeries.Last(i);

}

var avg1 = values1.Average();

var avg2 = values2.Average();

var sum = values1.Zip(values2, (x1, y1) => (x1 - avg1) * (y1 - avg2)).Sum();

var sumSqr1 = values1.Sum(x => Math.Pow((x - avg1), 2.0));

var sumSqr2 = values2.Sum(y => Math.Pow((y - avg2), 2.0));

return Math.Round(sum / Math.Sqrt(sumSqr1 * sumSqr2), 2);

}

This function returns the correlation between two data series.

@afhacker

afhacker

21 Jun 2018, 07:23

RE:

PapaGohan said:

Pivot points with sup/res is available on every other platform I have tried. Is this something in the works? Could it be added to some sort of "todo list"?

FX Trading Station has the ability to add 6 different types of pivot points:

- Classic pivot

- Camarilla

- Woodie

- Fibonacci

- Floor

- Fibonacci retracement

It's super useful, having anything like this built in would be great!

Five different types of pivot points indicator for cTrader: https://www.algodeveloper.com/product/pivot-points/

@afhacker

afhacker

13 Jun 2018, 15:01

RE:

Panagiotis Charalampous said:

Dear Trader,

Thanks for posting in our forum. This is currently not possible in cAlgo. A workaround is to get the Color as a string parameter and use the following function to convert the string to a Color

//A function for getting the color from a string private Colors GetColor(string colorString) { foreach (Colors color in Enum.GetValues(typeof(Colors))) { if (color.ToString() == colorString) return color; } return Colors.White; }Let me know if this helps,

Best Regards,

Panagiotis

Simple method:

private Colors GetColor(string colorText, string colorParameterName)

{

Colors color;

if (!Enum.TryParse(colorText, true, out color))

{

string errorObjName = string.Format("Your input for '{0}' parameter is incorrect", colorParameterName);

ChartObjects.DrawText("Error", errorObjName, StaticPosition.Center, Colors.Red);

// throw new ArgumentException(errorObjName);

}

return color;

}

@afhacker

afhacker

18 Mar 2018, 06:07

Supply and demand zones indicator for cTrader: https://www.algodeveloper.com/1-supply-and-demand-zones

@afhacker

afhacker

02 Mar 2018, 09:56

First thanks for adding this new features but what about community requests? where is multi-symbol backtesting? or different parameter types like Enums, date time picker,...

And is there any property to get a collection of all available symbols? that will be a simple feature to add before releasing the new version of API.

The current API library is based on .Net framework 4 which is obsolete, please update the .Net version to > 4.6 at least.

Another main issue of current API is limited drawing, please improve the API chart drawing feature by adding:

1. Transparency

2. Different shapes drawing

3. Checking current objects on chart and modifying those objects

4. A collection of objects drawn by current indicator or cBot

And please add a property to get the user platform (not system as it's available by .Net) time zone as a .Net TimeZoneInfo object.

Adding all these features will not get much time but I don't know why Spotware is very slow in adding new features?

Multi-symbol backtesting is one of the top suggestions and most voted of the community so please add it!

@afhacker

afhacker

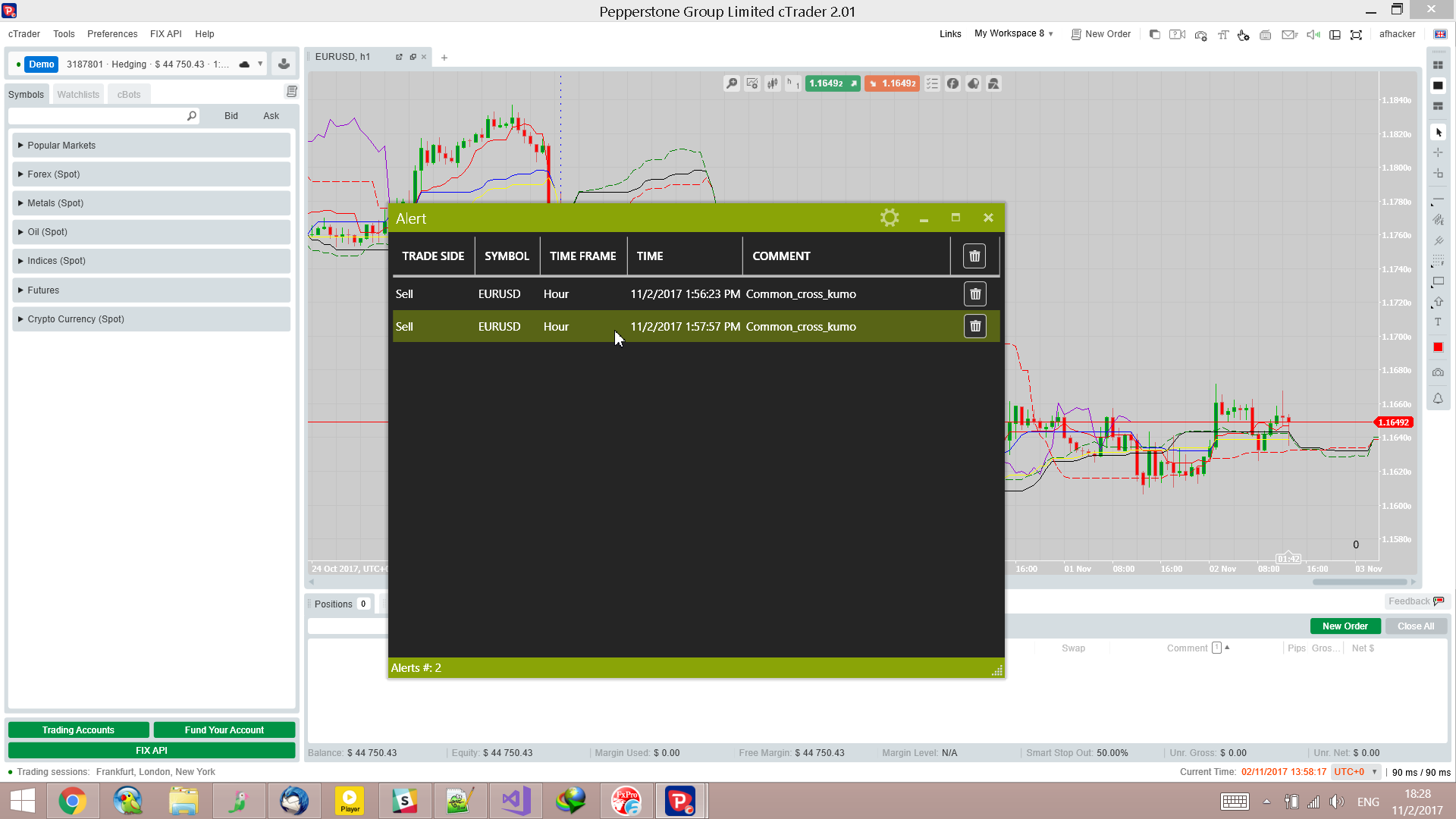

02 Nov 2017, 16:04

( Updated at: 21 Dec 2023, 09:20 )

Hi Hamid Reza,

There were some bugs in Alert library that I fixed and the new version is available, you can download your indicator which uses the new version of the alert library from here:

https://drive.google.com/open?id=0B93GK1Ip4NSMWldXRTljRTZ1ZEk

@afhacker

afhacker

31 Oct 2017, 17:28

You can download the compiled version of indicator from this link: https://drive.google.com/open?id=0B93GK1Ip4NSMdVVLbThRWjhMZmM

using System;

using cAlgo.API;

using cAlgo.API.Indicators;

using System.Threading.Tasks;

namespace cAlgo.Indicators

{

[Indicator(IsOverlay = true, TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)]

public class IchimokuKinkoHyo : Indicator

{

private int alertBarIndex = 0;

[Parameter(DefaultValue = 9)]

public int periodFast { get; set; }

[Parameter(DefaultValue = 26)]

public int periodMedium { get; set; }

[Parameter(DefaultValue = 52)]

public int periodSlow { get; set; }

[Parameter(DefaultValue = 26)]

public int DisplacementChikou { get; set; }

[Parameter(DefaultValue = 26)]

public int DisplacementCloud { get; set; }

[Parameter(DefaultValue = 26)]

public int Displacementkijunsen { get; set; }

[Parameter(DefaultValue = 0)]

public int Displacemenspanb { get; set; }

[Parameter("Text Color", DefaultValue = "Black")]

public string TextColor { get; set; }

[Parameter(DefaultValue = true)]

public bool Common_cross { get; set; }

[Parameter(DefaultValue = false)]

public bool Uncommon { get; set; }

[Parameter(DefaultValue = true)]

public bool Common_cross_kumo { get; set; }

[Output("TenkanSen", Color = Colors.Red)]

public IndicatorDataSeries TenkanSen { get; set; }

[Output("Kijunsen", Color = Colors.Blue)]

public IndicatorDataSeries KijunSen { get; set; }

[Output("ChikouSpan", Color = Colors.DarkViolet)]

public IndicatorDataSeries ChikouSpan { get; set; }

[Output("qualityline", Color = Colors.Black)]

public IndicatorDataSeries qualityline { get; set; }

[Output("SenkouSpanB", Color = Colors.Red, LineStyle = LineStyle.Lines)]

public IndicatorDataSeries SenkouSpanB { get; set; }

[Output("SenkouSpanA", Color = Colors.Green, LineStyle = LineStyle.Lines)]

public IndicatorDataSeries SenkouSpanA { get; set; }

[Output("Directionline", Color = Colors.Yellow)]

public IndicatorDataSeries Directionline { get; set; }

private Colors color = Colors.Black;

double maxfast, minfast, maxmedium, minmedium, maxslow, minslow, maxbig, minbig;

protected override void Initialize()

{

Alert.Manager.Indicator = this;

Alert.Manager.WindowTheme = Alert.Manager.Theme.BaseLight;

Alert.Manager.WindowAccent = Alert.Manager.Accent.Red;

Enum.TryParse(TextColor, out color);

}

public override void Calculate(int index)

{

if (IsLastBar)

DisplaySpreadOnChart();

if ((index < periodFast) || (index < periodSlow))

{

return;

}

string signalType = string.Empty;

maxfast = MarketSeries.High[index];

minfast = MarketSeries.Low[index];

maxmedium = MarketSeries.High[index];

minmedium = MarketSeries.Low[index];

maxbig = MarketSeries.High[index];

minbig = MarketSeries.Low[index];

maxslow = MarketSeries.High[index];

minslow = MarketSeries.Low[index];

for (int i = 0; i < periodFast; i++)

{

if (maxfast < MarketSeries.High[index - i])

{

maxfast = MarketSeries.High[index - i];

}

if (minfast > MarketSeries.Low[index - i])

{

minfast = MarketSeries.Low[index - i];

}

}

for (int i = 0; i < periodMedium; i++)

{

if (maxmedium < MarketSeries.High[index - i])

{

maxmedium = MarketSeries.High[index - i];

}

if (minmedium > MarketSeries.Low[index - i])

{

minmedium = MarketSeries.Low[index - i];

}

}

for (int i = 0; i < periodSlow; i++)

{

if (maxslow < MarketSeries.High[index - i])

{

maxslow = MarketSeries.High[index - i];

}

if (minslow > MarketSeries.Low[index - i])

{

minslow = MarketSeries.Low[index - i];

}

}

TenkanSen[index] = (maxfast + minfast) / 2;

KijunSen[index] = (maxmedium + minmedium) / 2;

ChikouSpan[index - DisplacementChikou] = MarketSeries.Close[index];

SenkouSpanA[index + DisplacementCloud] = (TenkanSen[index] + KijunSen[index]) / 2;

SenkouSpanB[index + DisplacementCloud] = (maxslow + minslow) / 2;

qualityline[index + Displacementkijunsen] = (maxmedium + minmedium) / 2;

Directionline[index] = (maxslow + minslow) / 2;

if (KijunSen[index] == TenkanSen[index] && Common_cross)

{

ChartObjects.DrawVerticalLine(index.ToString(), MarketSeries.OpenTime[index], Colors.Red, 1, LineStyle.DotsVeryRare);

ChartObjects.RemoveObject((index - 1).ToString());

TriggerAlert(TradeType.Sell, index, "Common_cross");

}

if (TenkanSen.HasCrossedAbove(KijunSen, 0) && Uncommon)

{

ChartObjects.DrawVerticalLine(index.ToString(), MarketSeries.OpenTime[index], Colors.Green, 1, LineStyle.DotsVeryRare);

ChartObjects.RemoveObject((index - 1).ToString());

TriggerAlert(TradeType.Sell, index, "Uncommon");

}

if (KijunSen[index] == TenkanSen[index] && SenkouSpanA[index + DisplacementCloud] == SenkouSpanB[index + DisplacementCloud] && Common_cross_kumo)

{

ChartObjects.DrawVerticalLine(index.ToString(), MarketSeries.OpenTime[index], Colors.Blue, 1, LineStyle.DotsVeryRare);

ChartObjects.RemoveObject((index - 1).ToString());

TriggerAlert(TradeType.Sell, index, "Common_cross_kumo");

}

}

private void DisplaySpreadOnChart()

{

var spread = Math.Round(Symbol.Spread / Symbol.PipSize, 2);

string text = string.Format("{0}", spread);

ChartObjects.DrawText("spread", "\t" + text, StaticPosition.BottomRight, Colors.Black);

}

private void TriggerAlert(TradeType alertType, int index, string msg)

{

if (index != alertBarIndex && IsLastBar && IsRealTime)

{

alertBarIndex = index;

Alert.Manager.Trigger(alertType, Symbol, MarketSeries.TimeFrame, Server.Time, msg);

}

}

}

}

@afhacker

afhacker

23 Oct 2018, 07:57

You can also use my Advanced Volume indicator, it counts each up/down tick of the last bar and shows it in two different up/down histogram bar.

For historical bars, it uses a formula to count the number of up/down ticks, you can find more detail on its description.

@afhacker