Topics

Replies

samuel.jus.cornelio

04 Aug 2020, 18:45

( Updated at: 21 Dec 2023, 09:22 )

RE:

PanagiotisCharalampous said:

PanagiotisCharalampous said:

Hi samuel.jus.cornelio,

Can you please write in English? It will be easier for us to help you. The code is a mess, did you just copy and paste stuff?

Best Regards,

Panagiotis

@samuel.jus.cornelio

samuel.jus.cornelio

04 Aug 2020, 17:00

RE:

PanagiotisCharalampous said:

Hi samuel.jus.cornelio,

Can you please write in English? It will be easier for us to help you. The code is a mess, did you just copy and paste stuff?

Best Regards,

Panagiotis

sorry, here is the translation of my post, thanks for your attention

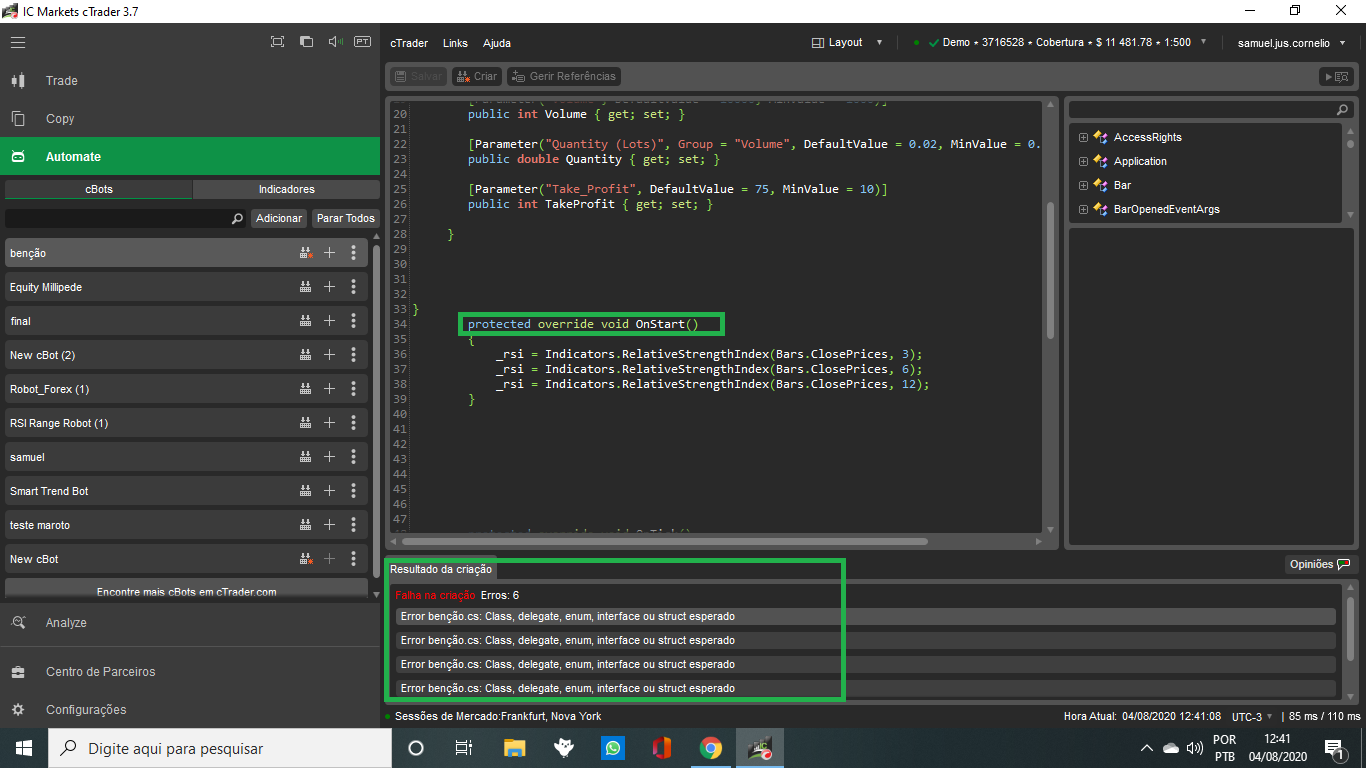

Hello guys, I have found some problems with my code and I can't find an answer to solve the problem. I am receiving an error warning regarding "VOID" it announces the error of "class delegate enum interface or expected struct" how can i solve this problem?

using System;

using System.Linq;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

using cAlgo.Indicators;

namespace cAlgo.Robots

{

[Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class NewcBot : Robot

{

[Parameter(DefaultValue = 0.0)]

public double Parameter { get; set; }

[Parameter("Stop Loss (pips)", DefaultValue = 10, MinValue = 1)]

public int StopLoss { get; set; }

[Parameter("Volume", DefaultValue = 10000, MinValue = 1000)]

public int Volume { get; set; }

[Parameter("Quantity (Lots)", Group = "Volume", DefaultValue = 0.02, MinValue = 0.01, Step = 0.01)]

public double Quantity { get; set; }

[Parameter("Take_Profit", DefaultValue = 75, MinValue = 10)]

public int TakeProfit { get; set; }

}

}

protected override void OnStart()

{

_rsi = Indicators.RelativeStrengthIndex(Bars.ClosePrices, 3);

_rsi = Indicators.RelativeStrengthIndex(Bars.ClosePrices, 6);

_rsi = Indicators.RelativeStrengthIndex(Bars.ClosePrices, 12);

}

protected override void OnTick()

{

if (_rsi.Result.LastValue < 40)

if (_rsi2.Result.LastValue < 40)

if (_rsi3.Result.LastValue < 40)

Close(TradeType.buy);

Open(TradeType.sell);

if (_rsi.Result.LastValue > 60)

if (_rsi2.Result.LastValue > 60)

if (_rsi3.Result.LastValue > 60)

Close(TradeType.Sell);

Open(TradeType.Buy);

}

protected override void OnStop()

{

private void Close(TradeType tradeType)

{

foreach (var position in Positions.FindAll("SampleRSI", Symbol, tradeType))

ClosePosition(position);

}

private void Open(TradeType tradeType)

{

var position = Positions.Find("SampleRSI", Symbol, tradeType);

if (position == null)

ExecuteMarketOrder(tradeType, Symbol, Volume, "SampleRSI");

}

}

}

}

@samuel.jus.cornelio

samuel.jus.cornelio

07 Aug 2020, 01:04 ( Updated at: 07 Aug 2020, 08:21 )

Hi guys, please. what is the correct way to place overbought and oversold parameters of the RSI? thank you for the kindness

[Parameter("Source")]

public DataSeries Source { get; set; }

[Parameter("Periods", DefaultValue = 14)]

public int Periods { get; set; }

[Parameter("overbought", DefaultValue < 60)]

public double overbought { get; set; }

[Parameter("oversold", DefaultValue > 40)]

public double oversold { get; set; }

@samuel.jus.cornelio