Topics

Replies

martin100181@gmail.com

11 Jul 2019, 18:10

RE:

Panagiotis Charalampous said:

Hi martin100181@gmail.com,

Why do you set -1 in Last() function? e.g. below

slowMa.Result.Last(-1)Best regards,

Panagiotis

That was a Mistake! thank you.

@martin100181@gmail.com

martin100181@gmail.com

11 Jul 2019, 17:19

( Updated at: 21 Dec 2023, 09:21 )

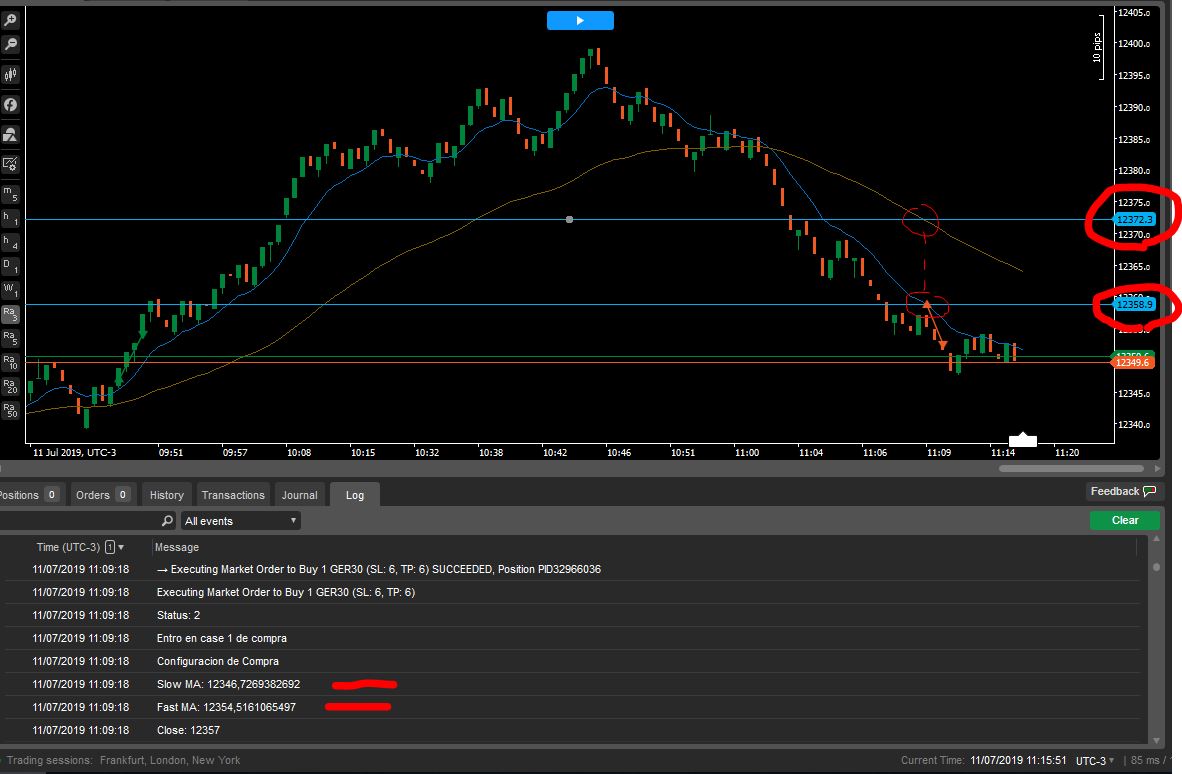

Also I discovered I´m getting wrong EMAs values. They don´t match the ones on chart. help please!!

@martin100181@gmail.com

martin100181@gmail.com

11 Jul 2019, 16:56

Maybe my code is not so good because I´m not a coder. The Idea is to make the bot trade when price make a retracement inside both EMAs and get out of them. Long or Short will depend on EMAs direction.

The way I find to make this was assigning a status code for the different stages of the cicle. Maybe there´s a much better way, of course.

@martin100181@gmail.com

martin100181@gmail.com

11 Jul 2019, 15:43

RE:

using System;

using System.Linq;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

using cAlgo.Indicators;

namespace cAlgo.Robots

{

[Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class FrankiRangetraderv1 : Robot

{

[Parameter("Source")]

public DataSeries SourceSeries { get; set; }

[Parameter("Slow Periods", DefaultValue = 50)]

public int SlowPeriods { get; set; }

[Parameter("Fast Periods", DefaultValue = 14)]

public int FastPeriods { get; set; }

[Parameter("Volumen", DefaultValue = 10000)]

public double volumen { get; set; }

[Parameter("TP", DefaultValue = 6)]

public double SL { get; set; }

[Parameter("SL", DefaultValue = 6)]

public double TP { get; set; }

public int status;

private ExponentialMovingAverage slowMa;

private ExponentialMovingAverage fastMa;

protected override void OnStart()

{

fastMa = Indicators.ExponentialMovingAverage(SourceSeries, FastPeriods);

slowMa = Indicators.ExponentialMovingAverage(SourceSeries, SlowPeriods);

status = 0;

}

protected override void OnBar()

{

int index = MarketSeries.Close.Count;

Print("------------------ New Bar ------------------");

Print("Close: " + MarketSeries.Close.Last(1));

Print("Fast MA: " + fastMa.Result.Last(1));

Print("Slow MA: " + slowMa.Result.Last(1));

if (slowMa.Result.Last(1) < fastMa.Result.Last(1))

{

Print("Configuracion de Compra");

switch (status)

{

case 0:

Print("Entro en case 0 de compra");

if (MarketSeries.Close.Last(1) > fastMa.Result.Last(1))

status = 0;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(1) && MarketSeries.Close.Last(1) > slowMa.Result.Last(1))

status = 1;

if (MarketSeries.Close.Last(1) < slowMa.Result.Last(1))

status = -1;

break;

case 1:

Print("Entro en case 1 de compra");

if (MarketSeries.Close.Last(1) > fastMa.Result.Last(1))

status = 2;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(1) && MarketSeries.Close.Last(1) > slowMa.Result.Last(1))

status = 1;

if (MarketSeries.Close.Last(1) < slowMa.Result.Last(1))

status = -1;

break;

case 2:

Print("Entro en case 2 de compra");

if (MarketSeries.Close.Last(1) > fastMa.Result.Last(1))

status = 0;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(1) && MarketSeries.Close.Last(1) > slowMa.Result.Last(1))

status = 1;

if (MarketSeries.Close.Last(1) < slowMa.Result.Last(1))

status = -1;

break;

case -1:

Print("Entro en case -1 de compra");

if (MarketSeries.Close.Last(1) > fastMa.Result.Last(1))

status = 0;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(1) && MarketSeries.Close.Last(1) > slowMa.Result.Last(1))

status = -1;

if (MarketSeries.Close.Last(1) < slowMa.Result.Last(1))

status = -1;

break;

}

Print("Status: " + status);

int Open_trades = Positions.Count(p => p.SymbolName == Symbol.Name);

int Open_orders = PendingOrders.Count(p => p.SymbolCode == Symbol.Name);

if (Open_trades == 0 && Open_orders == 0 && status == 2)

{

ExecuteMarketOrder(TradeType.Buy, Symbol, volumen, "Compra", SL, TP);

Print("Abre Compra");

}

{

}

}

if (slowMa.Result.Last(1) > fastMa.Result.Last(1))

{

Print("Configuración de Venta");

switch (status)

{

case 0:

Print("Entro en case 0 de venta");

if (MarketSeries.Close.Last(1) > slowMa.Result.Last(-1))

status = -1;

if (MarketSeries.Close.Last(1) <= slowMa.Result.Last(-1) && MarketSeries.Close.Last(1) >= fastMa.Result.Last(-1))

status = 1;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(-1))

status = 0;

break;

case 1:

Print("Entro en case 1 de venta");

if (MarketSeries.Close.Last(1) > slowMa.Result.Last(-1))

status = -1;

if (MarketSeries.Close.Last(1) < slowMa.Result.Last(-1) && MarketSeries.Close.Last(1) > fastMa.Result.Last(-1))

status = 1;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(-1))

status = 2;

break;

case 2:

Print("Entro en case 2 de venta");

if (MarketSeries.Close.Last(1) > slowMa.Result.Last(-1))

status = -1;

if (MarketSeries.Close.Last(1) < slowMa.Result.Last(-1) && MarketSeries.Close.Last(1) > fastMa.Result.Last(-1))

status = 1;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(-1))

status = 0;

break;

case -1:

Print("Entro en case -1 de venta");

if (MarketSeries.Close.Last(1) > slowMa.Result.Last(-1))

status = -1;

if (MarketSeries.Close.Last(1) < slowMa.Result.Last(-1) && MarketSeries.Close.Last(1) > fastMa.Result.Last(-1))

status = -1;

if (MarketSeries.Close.Last(1) < fastMa.Result.Last(-1))

status = 0;

break;

}

Print("Status: " + status);

int Open_trades = Positions.Count(p => p.SymbolName == Symbol.Name);

int Open_orders = PendingOrders.Count(p => p.SymbolCode == Symbol.Name);

if (Open_trades == 0 && Open_orders == 0 && status == 2)

{

ExecuteMarketOrder(TradeType.Sell, Symbol, volumen, "Venta", SL, TP);

Print("Status: " + status);

Print("Abre Venta");

}

}

Print("---------------------------------------------");

}

}

}

Panagiotis Charalampous said:

Hi martin100181@gmail.com,

Can you post the complete cBot code?

Best Regards,

Panagiotis

@martin100181@gmail.com

martin100181@gmail.com

25 Jun 2019, 23:32

Thank you Panagiotis.

Could you please take a look a this simple code? can´t find the error:

using System;

using System.Linq;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

using cAlgo.Indicators;

namespace cAlgo.Robots

{

[Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class Range_Franki_v1 : Robot

{

[Parameter(DefaultValue = 0.0)]

public double Parameter { get; set; }

[Parameter("Renko Pips", DefaultValue = 10)]

public double RenkoPips { get; set; }

public int BricksToShow = 100;

private Renko renko;

protected override void OnStart()

{

{

Print("ON-ST-(renko O;C) [", i, "]: ", MarketSeries.Open.Last(i), ";", MarketSeries.Close.Last(i));

}

}

protected override void OnTick()

{

// Put your core logic here

}

protected override void OnStop()

{

// Put your deinitialization logic here

}

}

}

@martin100181@gmail.com

martin100181@gmail.com

25 Jun 2019, 05:44

Also, when trying to use the indicator I get this error:

Error CS0246: The type or namespace name 'Renko' could not be found (are you missing a using directive or an assembly reference?)

How can I solve it?

@martin100181@gmail.com

martin100181@gmail.com

25 Jun 2019, 05:04

Dear Panagiotis,

is there any way to backtest with range bars or renko?

With built in range and renko I cant, is it possible somehow with an indicator?

BR

Martin

@martin100181@gmail.com

martin100181@gmail.com

10 Jun 2019, 23:48

More:

In fact I need the following:

1. I create a pending order with a defined target price and a label. Lets say "Long_1".

2. Sometime after that, it is possible that the bot stoped or whatever, so on the start I need the bot to check if Long_1 exists as a Pending order or if it was executed and its now a position and get the entry pice value (or target price if it´s still a pending order).

3. As a result I need to have that price stores in a variable.

I hope I could explain myself.

Thank you!

@martin100181@gmail.com

martin100181@gmail.com

11 Jul 2019, 18:12

RE:

Panagiotis Charalampous said:

I use default parameters.

GER30, Range bars 3 pips.

Slow EMA 50

Fast EMA 10

6 pips SL

6 pips TP

@martin100181@gmail.com