I get the same issue. If I compile my bot with SDK version 8, it works locally but crashes in the cloud. If I remove version 8 and install version 6, Ctrader does not see the version 6 SDK. To make matters worse, cloud sync has been hanging while synchronising for the last half hour, not sure how to resolve this issue.

Cwebhook

16 Dec 2024, 11:32

( Updated at: 17 Dec 2024, 07:44 )

Have a look at my new web app https://cwebhook.com it does exactly what you describe, also it is hosted in the same data centre TradingView use so trades get placed very fast.

Cwebhook

16 Dec 2024, 11:19

( Updated at: 17 Dec 2024, 07:44 )

Hello,

That is the exact usecase I needed personally, as an accomplished web dev I decided to build my own solution ‘Cwebhook’ based on the cTrader Open API, you can find out more about the service here: https://cwebhook.com it will work with any TradingView indicator that uses an alertcondition function.

I'm not sure what you want to do, but start with this approach, if you explain better what you want to achieve I can help you better

using cAlgo.API;using cAlgo.API.Indicators;using System;namespace cAlgo{ [Indicator(IsOverlay = true, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)] public class test : Indicator { protected override void Initialize() { SimpleMovingAverage sma = Indicators.SimpleMovingAverage(Bars.ClosePrices, 100); double body = Math.Abs(Bars.ClosePrices.Last(0) - Bars.OpenPrices.Last(0)); double body_sma = sma.Result.Last(0) * 3.0; } public override void Calculate(int index) { } } }

Thanks for the reply.

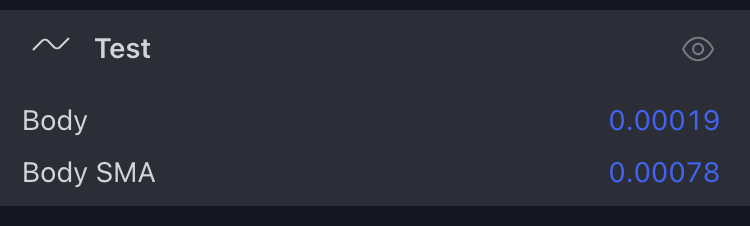

The body var returns a pip value of the current candle, in tradingview that pip value is passed directly to the sma function which then returns an average pip value, for example if I log the output to the data window these are those 2 values, which are changing in realtime with tick data. I'm trying to achieve the same in ctrader but no idea how to.

Cwebhook

12 Feb 2025, 20:32

I get the same issue. If I compile my bot with SDK version 8, it works locally but crashes in the cloud. If I remove version 8 and install version 6, Ctrader does not see the version 6 SDK. To make matters worse, cloud sync has been hanging while synchronising for the last half hour, not sure how to resolve this issue.

@Cwebhook