Using candle body range as source for SimpleMovingAverage

05 Jan 2024, 09:43

Hello, I am new to cTrader having used TradingView for a number of years. I am having difficulty converting the simple pinescript code shown below over to ctrader.

I have so far:

var bar = Bars[0];

var body = Math.Abs(bar.Close - bar.Open);

but if I try to do:

var body_sma = Indicators.SimpleMovingAverage(body, 100) * 3.0;

I get the error: cannot convert from ’double' to ‘cAlgo.API.DataSeries’

How would I go about replicating the sma value?

indicator('Test', overlay=true)

body = math.abs(close - open)

body_sma = ta.sma(body, 100) * 3.0

buy = false

if close < open and body > body_sma

buy := true

plotshape(buy, style=shape.arrowup, color=color.new(color.green, 0), location=location.belowbar)

I'm not sure what you want to do, but start with this approach, if you explain better what you want to achieve I can help you better

using cAlgo.API;using cAlgo.API.Indicators;using System;namespace cAlgo{ [Indicator(IsOverlay = true, TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)] public class test : Indicator { protected override void Initialize() { SimpleMovingAverage sma = Indicators.SimpleMovingAverage(Bars.ClosePrices, 100); double body = Math.Abs(Bars.ClosePrices.Last(0) - Bars.OpenPrices.Last(0)); double body_sma = sma.Result.Last(0) * 3.0; } public override void Calculate(int index) { } } }

Thanks for the reply.

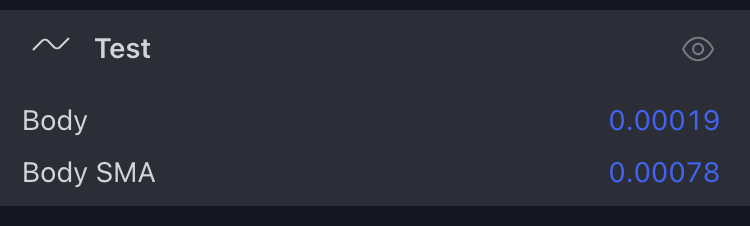

The body var returns a pip value of the current candle, in tradingview that pip value is passed directly to the sma function which then returns an average pip value, for example if I log the output to the data window these are those 2 values, which are changing in realtime with tick data. I'm trying to achieve the same in ctrader but no idea how to.

I think I understand, you don't need to manipulate the SMA, you can recreate it, this is a simple example:

using System;

using cAlgo.API;

using cAlgo.API.Internals;

namespace cAlgo

{

[Indicator(IsOverlay = false, AccessRights = AccessRights.None)]

[Levels(0.0005)]

public class BodySMA : Indicator

{

[Parameter("Period", DefaultValue = 10, MinValue = 2)]

public int Period { get; set; }

[Output("Average", LineColor = "DodgerBlue")]

public IndicatorDataSeries Average { get; set; }

protected override void Initialize()

{

// TODO

}

public override void Calculate(int index)

{

if (index < Period) return;

double sum = 0;

for (int i = index - Period + 1; i <= index; i++)

{

sum += Math.Abs( Bars.ClosePrices[i] - Bars.OpenPrices[i]);

}

Average[index] = Math.Round( sum / Period, Symbol.Digits);

}

}

}

ctrader.guru

05 Jan 2024, 12:14

I'm not sure what you want to do, but start with this approach, if you explain better what you want to achieve I can help you better

@ctrader.guru