Empty tick data, how to create TDBC files?

Replies

trend_meanreversion

30 Dec 2015, 12:10

( Updated at: 21 Dec 2023, 09:20 )

RE: RE: RE:

DeletedUser said:

Hi Simon,

You can try different broker to get data for Index CFDs. Very few brokers are providing tick data for FX + Index CFDs. Some of them don't even provide tick data for FX pairs. In any case, try on ICMarkets to get tick data for index CFDs.

@trend_meanreversion

.ics

31 Dec 2015, 06:04

( Updated at: 23 Aug 2022, 15:24 )

RE: RE:

DeletedUser said:

Hi Paul,

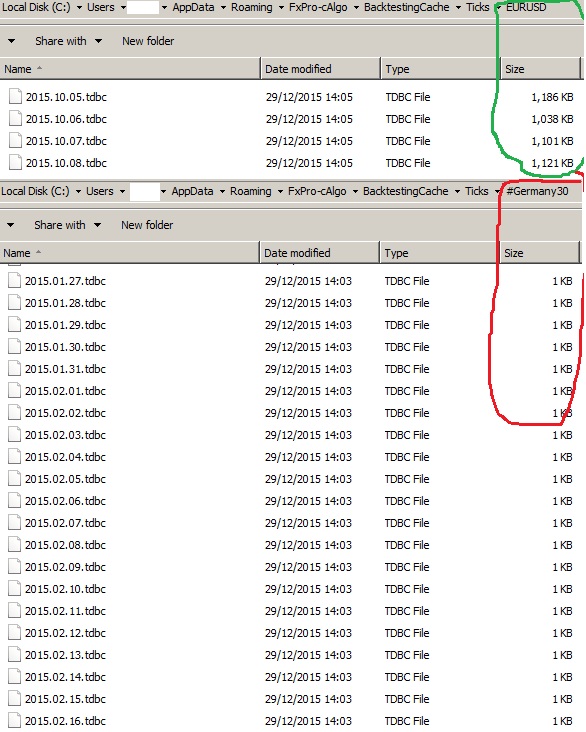

Thanks for the response, I currently have 1m bars from a csv file working with backtesting, and some tick data is working for certain symbols (EURUSD etc), however for the symbol I need most (Germany30), my broker is sending me empty data files (C:\Users\username\AppData\Roaming\FxPro-cAlgo\BacktestingCache\Ticks\#Germany30) are all empty 1KB files, as opposed to 1MB+ files for EURUSD data files

While testing 1 minute and greater algorithms is fine, it's annoying as my robot is designed to handle orders down to the tick

And there's no chance for me to develop per tick based algorithms by backtesting, only via watching the market live

It's should be an easy problem to resolve, but my broker doesn't seem to understand the issue yet, so I was hoping Spotware might be able to resolve the issue

Hi Simon,

If you mention that some tick data is working for certain symbols, do you mean the tick data available from the broker server, or do you mean the tick data from dukascopy?

In case of tick data from dukascopy, could you share us how you are getting this tick data to work in cAlgo? This would make algo development more reliable because more historical data would be available for the algo testing.

Thanks in advance.

@.ics

.ics

02 Jan 2016, 00:30

( Updated at: 23 Aug 2022, 15:23 )

RE:

DeletedUser said:

Hi .ics,

Following trend_meanreversion's suggestion I downloaded the tick data using a demo ICMarkets account. Unfortunately I still don't know how to use the dukascopy tick data in cAlgo. If Spotware could direct us on how the TDBC files are formatted we could be able to do it. Or even better let us directly load tick data via CSV file. Sorry I can't be of more help.

Following on, some things are still a mystery to me, like when backtesting using tick data, there is no TimeFrame.Tick1, whereas live I can use MarketData.GetSeries(Symbol,this.TimeFrame), with timeframe being set to t1, thus letting me use indicators on tick data. This could just be me being stupid and just how it's meant to be, anyway I'm confused. At least now I can access tick data for backtesting.

Hi Simon,

Thanks for your clarification. It seems that we all are searching and waiting for the same feature in cAlgo. Being able to use more tick data than that now is provided.

Also, Happy New year! :)

@.ics

ClickAlgo

30 Dec 2015, 08:41

Hello Simon,

Just write a utility program that opens the CSV file and converts it to the format required for cTrader, unfortunately back testing will only accept 1m bars of data and not Tick data, you could try a small sample of tick data and see what happens.

Look at using the LINQ2CSV Library to read/write CSV files, its very simple to use.

It needs to be in the following format for cTrader import.

CSV file format

Example:

2003.06.18,16:01,1.11423,1.11428,1.11332,1.11374,19

2003.06.18,16:02,1.11364,1.11436,1.11361,1.11405,7

2003.06.18,16:03,1.11402,1.11455,1.11400,1.11440,5

2003.06.18,16:04,1.11446,1.11461,1.11401,1.11447,14

@ClickAlgo