Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

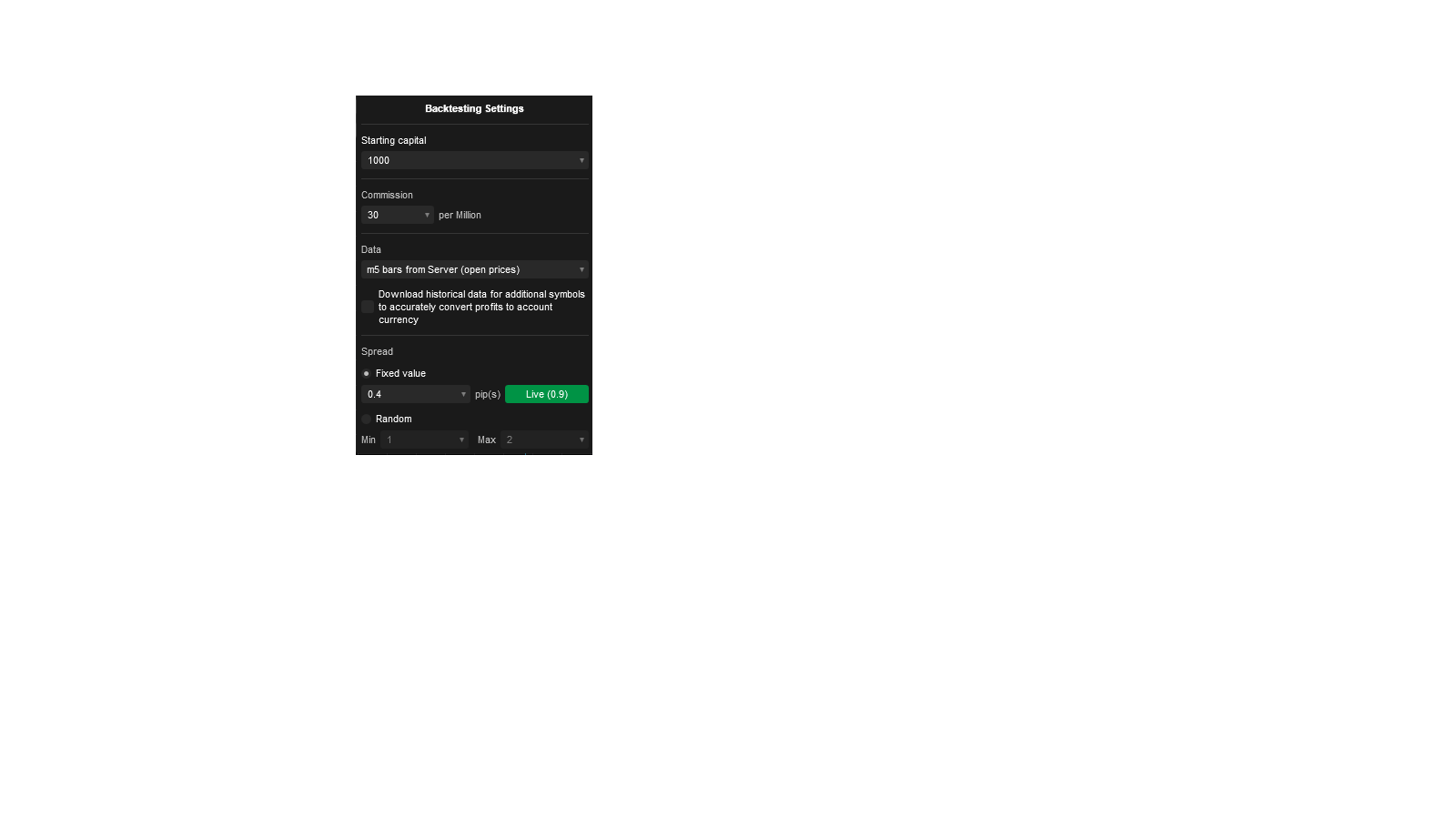

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed makes no sense to me.

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

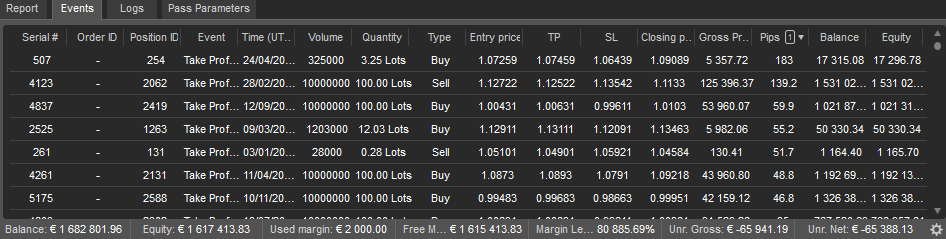

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Hi there,

I cannot provide an explanation of what you are looking at since I do not have your cBot's code. If you can help me reproduce what you are looking at, I will explain what happens. But I am 100% sure that this is not related with inaccurate executions. I am using cTrader for the last 8 years, I backtest several cBots every day and I can confirm that the execution with tick data is exact.

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Hi there,

I cannot provide an explanation of what you are looking at since I do not have your cBot's code. If you can help me reproduce what you are looking at, I will explain what happens. But I am 100% sure that this is not related with inaccurate executions. I am using cTrader for the last 8 years, I backtest several cBots every day and I can confirm that the execution with tick data is exact.

Best regards,

Panagiotis

Bot Code:

using System;

using System.Collections.Generic;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo.Robots

{

[Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)]

public class TradingBot : Robot

{

[Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 20)]

public double RiskPercentage { get; set; }

[Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)]

public double StopLossPips { get; set; }

[Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)]

public double TakeProfitPips { get; set; }

private AI_101.ML101.ModelInput _modelInput;

private double _lastPrediction;

protected override void OnStart()

{

_modelInput = new AI_101.ML101.ModelInput();

}

protected override void OnTick()

{

// Ensure only one open position per currency pair

if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0)

return;

// Update model input with the latest close price

_modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid

// Get prediction

var prediction = AI_101.ML101.Predict(_modelInput);

// Calculate the predicted price change

double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice;

// Determine if we should open a position

if (Math.Abs(predictedChange) > Symbol.PipSize)

{

if (predictedChange > 0 && _lastPrediction <= 0)

{

OpenPosition(TradeType.Buy);

}

else if (predictedChange < 0 && _lastPrediction >= 0)

{

OpenPosition(TradeType.Sell);

}

}

_lastPrediction = predictedChange;

}

private void OpenPosition(TradeType tradeType)

{

// Calculate position size based on risk

double riskAmount = Account.Balance * (RiskPercentage / 100);

double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue);

// Ensure volume is within acceptable range and increments

volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest);

// Check if the volume is valid

if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax)

{

Print("Volume is out of range: " + volumeInUnits);

return;

}

// Open the position

ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips);

}

}

}

I tried to optimize AUD/USD this time. Here is a link to my .optres file: https://file.io/JbtHJixXfPja

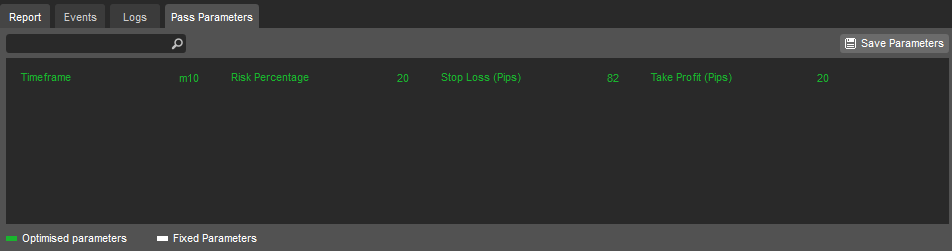

otherwise here is a documentation of “Report”, "Events" and “Paramaters” of my optimizer:

As you can see I used tick data, the parameters are set to SL/TP= 69/90 which are not met if I sort it by “Pips”

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Hi there,

I cannot provide an explanation of what you are looking at since I do not have your cBot's code. If you can help me reproduce what you are looking at, I will explain what happens. But I am 100% sure that this is not related with inaccurate executions. I am using cTrader for the last 8 years, I backtest several cBots every day and I can confirm that the execution with tick data is exact.

Best regards,

Panagiotis

Bot Code:

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 20)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

I tried to optimize AUD/USD this time. Here is a link to my .optres file: https://file.io/JbtHJixXfPja

otherwise here is a documentation of “Report”, "Events" and “Paramaters” of my optimizer:

As you can see I used tick data, the parameters are set to SL/TP= 69/90 which are not met if I sort it by “Pips”

Unfortunately I cannot run your code without this part

_modelInput = new AI_101.ML101.ModelInput();

If you can reproduce the issue without this line of code, I am more than happy to have a look

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Hi there,

I cannot provide an explanation of what you are looking at since I do not have your cBot's code. If you can help me reproduce what you are looking at, I will explain what happens. But I am 100% sure that this is not related with inaccurate executions. I am using cTrader for the last 8 years, I backtest several cBots every day and I can confirm that the execution with tick data is exact.

Best regards,

Panagiotis

Bot Code:

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 20)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

I tried to optimize AUD/USD this time. Here is a link to my .optres file: https://file.io/JbtHJixXfPja

otherwise here is a documentation of “Report”, "Events" and “Paramaters” of my optimizer:

As you can see I used tick data, the parameters are set to SL/TP= 69/90 which are not met if I sort it by “Pips”

Unfortunately I cannot run your code without this part

_modelInput = new AI_101.ML101.ModelInput();

If you can reproduce the issue without this line of code, I am more than happy to have a look

This is the link to the Ai#101 Module and my csv file:

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Hi there,

I cannot provide an explanation of what you are looking at since I do not have your cBot's code. If you can help me reproduce what you are looking at, I will explain what happens. But I am 100% sure that this is not related with inaccurate executions. I am using cTrader for the last 8 years, I backtest several cBots every day and I can confirm that the execution with tick data is exact.

Best regards,

Panagiotis

Bot Code:

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 20)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

I tried to optimize AUD/USD this time. Here is a link to my .optres file: https://file.io/JbtHJixXfPja

otherwise here is a documentation of “Report”, "Events" and “Paramaters” of my optimizer:

As you can see I used tick data, the parameters are set to SL/TP= 69/90 which are not met if I sort it by “Pips”

Unfortunately I cannot run your code without this part

_modelInput = new AI_101.ML101.ModelInput();

If you can reproduce the issue without this line of code, I am more than happy to have a look

This is the link to the Ai#101 Module and my csv file:

https://file.io/JbtHJixXfPja

I am not able to open this. In any case, if there is an issue with cTrader, this module is irrelevant. You would be able to reproduce it without it

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Hi there,

I cannot provide an explanation of what you are looking at since I do not have your cBot's code. If you can help me reproduce what you are looking at, I will explain what happens. But I am 100% sure that this is not related with inaccurate executions. I am using cTrader for the last 8 years, I backtest several cBots every day and I can confirm that the execution with tick data is exact.

Best regards,

Panagiotis

Bot Code:

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 20)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

I tried to optimize AUD/USD this time. Here is a link to my .optres file: https://file.io/JbtHJixXfPja

otherwise here is a documentation of “Report”, "Events" and “Paramaters” of my optimizer:

As you can see I used tick data, the parameters are set to SL/TP= 69/90 which are not met if I sort it by “Pips”

Unfortunately I cannot run your code without this part

_modelInput = new AI_101.ML101.ModelInput();

If you can reproduce the issue without this line of code, I am more than happy to have a look

This is the link to the Ai#101 Module and my csv file:

https://file.io/JbtHJixXfPja

I am not able to open this. In any case, if there is an issue with cTrader, this module is irrelevant. You would be able to reproduce it without it

I am not sure what you mean with reproducing?

I used it on my local machine and on an other virtual machine. In both cases I had the same wrong SL/TP results.

Please share your cBot code and make sure you are using tick data for your backtests.

Best regards,

Panagiotis

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 10)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

My thought was:

Since I collected only m5 candle data for my Machine learning module I changed the “Data” in settings to “m5 bars from server” for backtesting

and I was considering to change “protected override void OnTick()” to "protected override void OnBar()".

Is that wrong?

What is the best solution?

Thank you

Hi there,

If you are using fixed SL and TP, you need to use tick data to ensure accurate results in backtesting.

Best regards,

Panagiotis

Okay, my cbot code uses

protected override void OnTick()

I still get wrong TP.

You need to use tick data on your backtesting settings. OnTick() is irrelevant.

Where does the option “m5 bars from server” come from?

I thought the system provided the best possible set-up because of my csv file, which contains only m5 bars data.

I don't understand what you mean. It's just an option in a dropdown list

My friend,

I created a csv file with m5 bars only to train my module. I thought that is why I the option “M5” is available.

Can you please explain why in any of the options in Backtesting drop-down list is not triggering my predefined TP or SL .

What is the point of predefining it?

I thought the Backtesting process should prepare for the real environment. But when there are options which are not correctly executed by the system makes no sense to me.

The options have nothing to do with the data you used to generate the model. The backtesting module has no clue what your cBot is doing. Those options are there to choose the data source to be used for the backtesting. If you don't use tick data but you use SP and TP at specific price levels, your execution will be inaccurate, since m5 bars data source only uses open prices for the execution

Hi, ok I tried the optimizer with tick data from server.

The Optimizers choice of parameters : SL = 82; TP = 20

And this was the result. Again the TP was not correct: way more than 20 pips TP

I dont know mate. It seems to me there is no point of “testing” if the system doesnt TP/SL properly.

Hi there,

I cannot provide an explanation of what you are looking at since I do not have your cBot's code. If you can help me reproduce what you are looking at, I will explain what happens. But I am 100% sure that this is not related with inaccurate executions. I am using cTrader for the last 8 years, I backtest several cBots every day and I can confirm that the execution with tick data is exact.

Best regards,

Panagiotis

Bot Code:

using System;using System.Collections.Generic;using cAlgo.API;using cAlgo.API.Indicators;using cAlgo.API.Internals;namespace cAlgo.Robots{ [Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FullAccess)] public class TradingBot : Robot { [Parameter("Risk Percentage", DefaultValue = 1, MinValue = 0.1, MaxValue = 20)] public double RiskPercentage { get; set; } [Parameter("Stop Loss (Pips)", DefaultValue = 40, MinValue = 0, MaxValue = 100)] public double StopLossPips { get; set; } [Parameter("Take Profit (Pips)", DefaultValue = 20, MinValue = 0, MaxValue = 200)] public double TakeProfitPips { get; set; } private AI_101.ML101.ModelInput _modelInput; private double _lastPrediction; protected override void OnStart() { _modelInput = new AI_101.ML101.ModelInput(); } protected override void OnTick() { // Ensure only one open position per currency pair if (Positions.FindAll("ML Prediction", Symbol.Name).Length > 0) return; // Update model input with the latest close price _modelInput.ClosePrice = (float)Symbol.Bid; // Use Symbol.Bid instead of Symbol.LastTick.Bid // Get prediction var prediction = AI_101.ML101.Predict(_modelInput); // Calculate the predicted price change double predictedChange = prediction.ClosePrice[0] - _modelInput.ClosePrice; // Determine if we should open a position if (Math.Abs(predictedChange) > Symbol.PipSize) { if (predictedChange > 0 && _lastPrediction <= 0) { OpenPosition(TradeType.Buy); } else if (predictedChange < 0 && _lastPrediction >= 0) { OpenPosition(TradeType.Sell); } } _lastPrediction = predictedChange; } private void OpenPosition(TradeType tradeType) { // Calculate position size based on risk double riskAmount = Account.Balance * (RiskPercentage / 100); double volumeInUnits = riskAmount / (StopLossPips * Symbol.PipValue); // Ensure volume is within acceptable range and increments volumeInUnits = Symbol.NormalizeVolumeInUnits(volumeInUnits, RoundingMode.ToNearest); // Check if the volume is valid if (volumeInUnits < Symbol.VolumeInUnitsMin || volumeInUnits > Symbol.VolumeInUnitsMax) { Print("Volume is out of range: " + volumeInUnits); return; } // Open the position ExecuteMarketOrder(tradeType, Symbol.Name, volumeInUnits, "ML Prediction", StopLossPips, TakeProfitPips); } }}

I tried to optimize AUD/USD this time. Here is a link to my .optres file: https://file.io/JbtHJixXfPja

otherwise here is a documentation of “Report”, "Events" and “Paramaters” of my optimizer:

As you can see I used tick data, the parameters are set to SL/TP= 69/90 which are not met if I sort it by “Pips”

Unfortunately I cannot run your code without this part

_modelInput = new AI_101.ML101.ModelInput();

If you can reproduce the issue without this line of code, I am more than happy to have a look

This is the link to the Ai#101 Module and my csv file:

https://file.io/JbtHJixXfPja

I am not able to open this. In any case, if there is an issue with cTrader, this module is irrelevant. You would be able to reproduce it without it

I am not sure what you mean with reproducing?

I used it on my local machine and on an other virtual machine. In both cases I had the same wrong SL/TP results.

I mean that this should happen on other cBots as well. If you are able to provide a cBot and parameters that we can run, I will explain to you what happens. At the moment I cannot reproduce such behavior

zytotoxiziteat

31 Aug 2024, 13:02 ( Updated at: 31 Aug 2024, 13:03 )

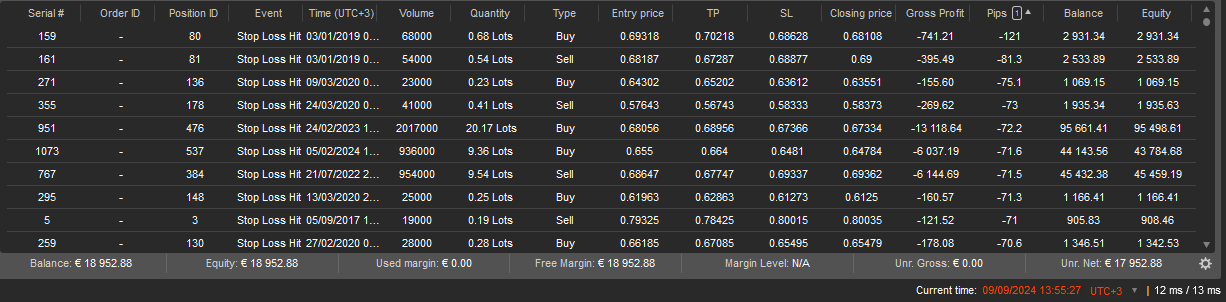

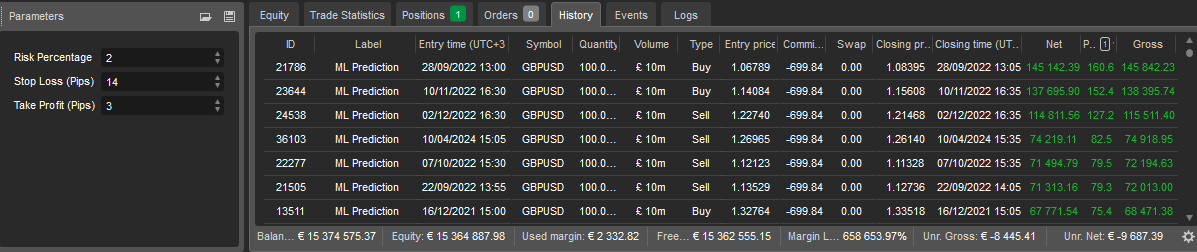

After retesting and sorting the values by pips I received this:

>>>160<<< Pips Take Profit ?!?!!?

How can ctrader take 160 pips profit when the parameter is clearly set on 3 ????

Can anyone explain this to me please?!

@zytotoxiziteat