Huge discrepancy in backtest results

Huge discrepancy in backtest results

05 Jun 2023, 19:36

Hey all,

I'm seeing an incredible discrepancy in the results of my strategy when running it with the 1m timeframe Vs the Tick data. I'm relatively new, so I was wondering if anyone could help explain why it's such a huge difference? The win rate and number of trades looks relatively similar, so I just don't see how we could have ended up with such a difference!

And, perhaps more importantly, if it's so inaccurate, doesn't this render the 1m backtesting entirely pointless?

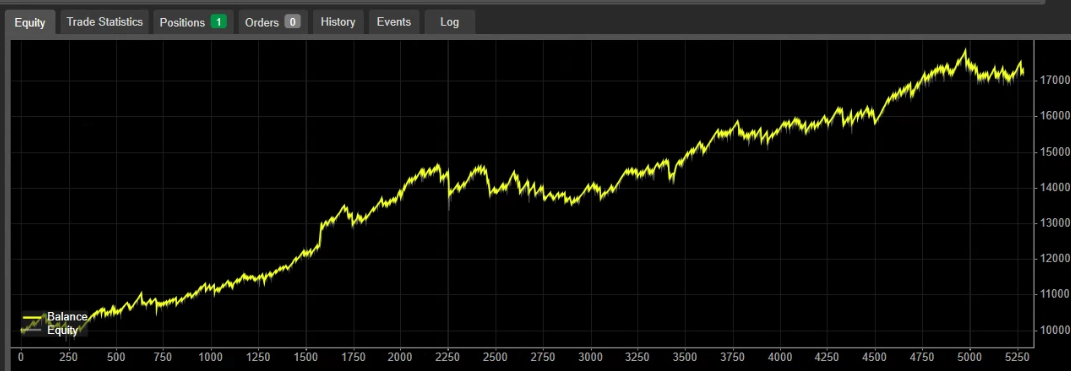

See screenshot below how my strategy terms from incredible.... to incredibly awful. All thoughts welcome!

Replies

PanagiotisChar

06 Jun 2023, 08:24

Hi lookitsben,

m1 data should only be used for strategies that are executed on each bar. For strategies that do stuff in OnTick or use pending orders, stop losses and take profits, m1 bars will be from slightly to completely inaccurate.

Need help? Join us on Telegram

Need premium support? Trade with us

@PanagiotisChar

lookitsben

06 Jun 2023, 11:09

RE:

PanagiotisChar said:

Hi lookitsben,

m1 data should only be used for strategies that are executed on each bar. For strategies that do stuff in OnTick or use pending orders, stop losses and take profits, m1 bars will be from slightly to completely inaccurate.

Need help? Join us on Telegram

Need premium support? Trade with us

Makes sense! Very helpful, thank you!!

@lookitsben

lookitsben

06 Jun 2023, 11:10

RE:

firemyst said:

When you back test do you take into account spreads and commission costs?

I thought these were included by default/built into the backtesting tool?

@lookitsben

imb24

06 Jun 2023, 14:05

RE: RE:

lookitsben said:

PanagiotisChar said:

Hi lookitsben,

m1 data should only be used for strategies that are executed on each bar. For strategies that do stuff in OnTick or use pending orders, stop losses and take profits, m1 bars will be from slightly to completely inaccurate.

Need help? Join us on Telegram

Need premium support? Trade with us

Makes sense! Very helpful, thank you!!

No, this does not make 100% sense ;-)

I have the same problem and created this topic:

The backtest simulator can do easily much better than it currently does. Checkout my example - imho this is clearly a sign of a bug.

@imb24

firemyst

06 Jun 2023, 08:04

When you back test do you take into account spreads and commission costs?

@firemyst