How I save my optimsation runs

How I save my optimsation runs

14 Jul 2022, 07:49

Hi all,

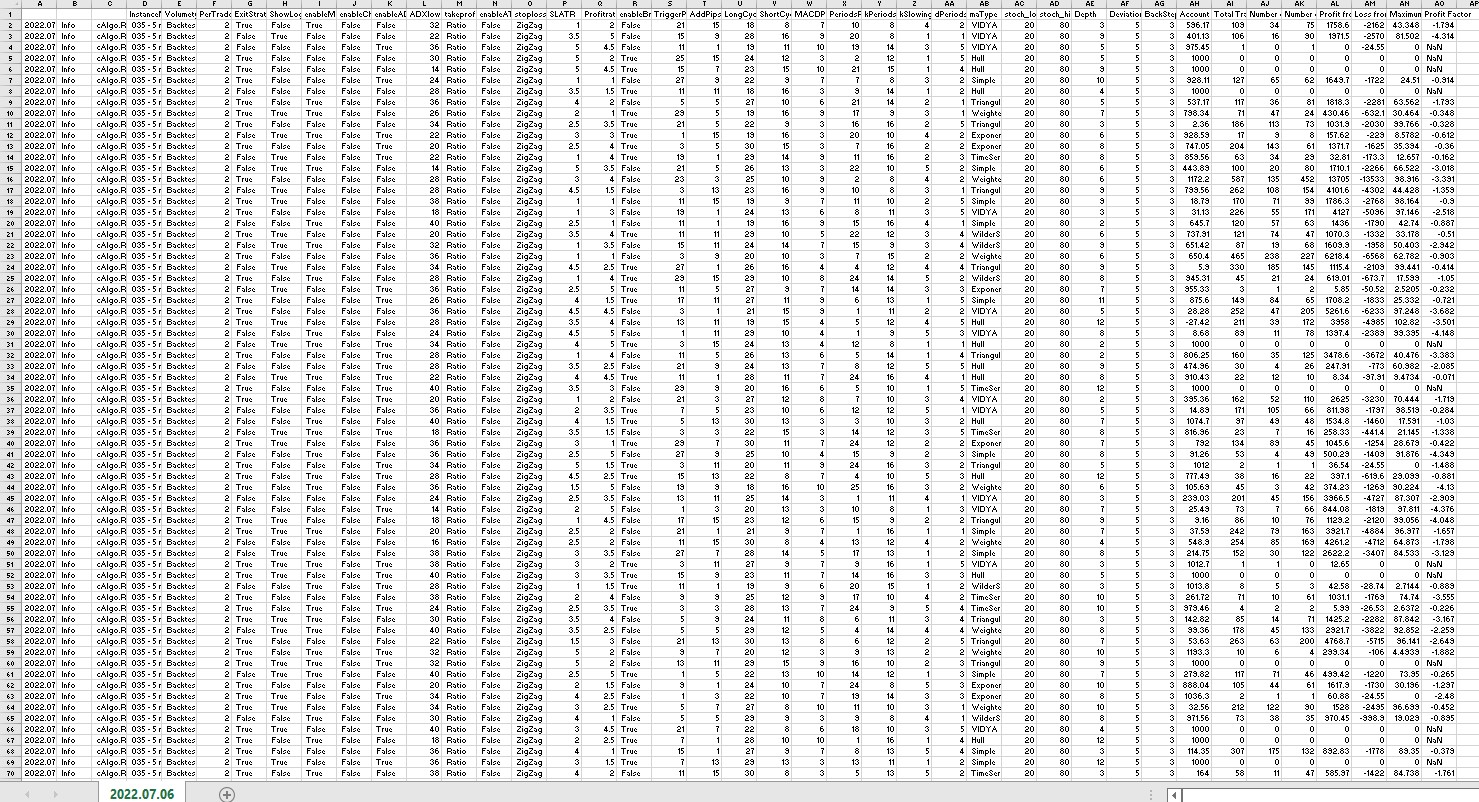

I am always asking for help, so thought I might be able to help someone else for a change. I have been doing some work on improving my use of optimsation runs and apart of that is saving them and analysing etc etc.

so this is how I do it. Please let me know if you have any questions etc, it gives good output but there is some mucking around to get it.

First I installed the cTrader CSV Data Export Tool from ClickAlgo. www.clickalgo.com/data-export-tool - do all the things need to get it to work etc etc.

Then I have put code into the "onstop()" part of my cbot to fetch all the information that I want. This way each time an optimsation run is completed, it sends that information to the spreadsheet.

For the " TradeLogger.Info(string.Concat(InstanceName.ToString(), etc " really long part I used a backtest run and then saved the parameters to a txt file. From there I put it into excel and use a CONCATENATEMULTIPLE function which I found (www.trumpexcel.com/concatenate-excel-ranges/) to make the list work.

If you send information to individual TradeLogger.Info it seems to get a bit mixed up and I couldnt ganurantee if all the parameters were from the same run, hence the giant line of code to get them all into one big string, then I separate them through the use of CSV. It is still a work in prgoress, so please let me know of any improvements. Currently I am working on system for forward testing and comparing them using some of the techniques from Darwinex's videos on youtube.

Here are the sections from my code.

//// parameters bit

[Parameter("Show Log FIle", Group = "Trade Logger", DefaultValue = false)]

public bool ShowLogFile { get; set; }

[Parameter("Enable Data Logger", Group = "Trade Logger", DefaultValue = false)]

public bool enableDataLogger { get; set; }

/// indicator declaration

// Trade logger stuff

private double peak;

private List<double> drawdown = new List<double>();

private List<string> individualtrades = new List<string>();

private double maxDrawdown;

//// onstart section

//trade logger stuff

Positions.Closed += PositionsOnClosed;

TradeLogger.SetLogDir("c:\\Users\\ianlo\\OneDrive\\Documents\\cAlgo\\Backtesting");

TradeLogger.Extension = "csv";

//// on stop section

protected override void OnStop()

{

if (enableDataLogger)

{

double calcs = Account.Balance;

double maxDD = GetMaxDrawDown();

int totaltrades = History.Count;

double winningtrades = winningtradesamount();

double losingtrades = totaltrades - winningtrades;

double profitfromwinning = winningtradestotal();

double Lossfromlosing = losingtradestotal();

//double profitfactor = (profitfromwinning / winningtrades) / (Lossfromlosing / losingtrades);

double profitfactor = ((winningtrades / totaltrades) * (profitfromwinning / winningtrades)) / ((losingtrades / totaltrades) * Math.Abs((Lossfromlosing / losingtrades)));

//int[] InvTrades = Equitycurve(ref cal).ToArray();

//string InvTradesString = string.Join(".", InvTrades);

TradeLogger.Info(string.Concat(InstanceName.ToString(), ", ", Volumetype.ToString(), ", ", PerTrade.ToString(), ", ", PeriodsST1.ToString(), ", ", MutliplierST1.ToString(), ", ", PeriodsST2.ToString(), ", ", MutliplierST2.ToString(), ", ", PeriodsST3.ToString(), ", ", MutliplierST3.ToString(), ", ", SLATR.ToString(), ", ", Profitratio.ToString(), ", ", PeriodsRSI.ToString(), ", ", RSIOverSold.ToString(), ", ", RSIOverBought.ToString(), ", ", enableChaikinfilter.ToString(), ", ", enableADXfilter.ToString(), ", ", ADXlow.ToString(), ", ", IncludeBreakEven.ToString(), ", ", BreakEvenPips.ToString(), ", ", BreakEvenExtraPips.ToString(), ", ", Profitratio.ToString(), ", ", calcs.ToString(), ", ", totaltrades.ToString(), ", ", winningtrades.ToString(), ", ", losingtrades.ToString(), ", ", profitfromwinning.ToString(), ", ", Lossfromlosing.ToString(), ", ", maxDD.ToString(), ", ", profitfactor.ToString()));

//TradeLogger.Info("Individual Trades " + InvTradesString);

}

}

////// private subs and PositiononClosed section ( I am still working on to make it better etc...)

#region Trade Logger and Get Fitness

private void PositionsOnClosed(PositionClosedEventArgs args)

{

var position = args.Position;

if (position.Label != InstanceName) return;

Print("Position labeled {0} has closed", position.Label);

GetMaxDrawDown();

var stringnetprofit = position.NetProfit;

Equitycurve(ref stringnetprofit);

}

private List<string> Equitycurve(ref double netprofit)

{

{

//List<string> individualtrades = new List<string>(); - add this back at the start

var stringnetprofit = netprofit.ToString();

individualtrades.Add(stringnetprofit);

return individualtrades;

//string[] InvTrades = individualtrades.ToArray();

//return InvTrades[];

// You can convert it back to an array if you would like to

//int[] terms = termsList.ToArray();

//string res = string.Join(".", str);

}

}

private double GetMaxDrawDown()

{

peak = Math.Max(peak, Account.Balance);

drawdown.Add((peak - Account.Balance) / peak * 100);

drawdown.Sort();

return maxDrawdown = drawdown[drawdown.Count - 1];

}

private double winningtradesamount()

{

double totalprofit = 0;

double gainedPips = 0;

int winningTrades = 0;

foreach (HistoricalTrade trade in History)

{

if (trade.Label == InstanceName)

{

totalprofit += trade.NetProfit;

gainedPips += trade.Pips;

if (trade.NetProfit > 0)

winningTrades++;

}

}

return winningTrades;

}

private double winningtradestotal()

{

double totalprofit = 0;

foreach (HistoricalTrade trade in History)

{

if (trade.Label == InstanceName)

{

if (trade.NetProfit > 0)

totalprofit += trade.NetProfit;

}

}

return totalprofit;

}

private double losingtradestotal()

{

double totalprofit = 0;

foreach (HistoricalTrade trade in History)

{

if (trade.Label == InstanceName)

{

if (trade.NetProfit < 0)

totalprofit += trade.NetProfit;

}

}

return totalprofit;

}

private double _fit_winLossRatio(GetFitnessArgs args)

{

double calcs = Account.Balance;

return args.WinningTrades / (args.WinningTrades + args.LosingTrades + 1);

}

#endregion