please convert this method

please convert this method

11 Jul 2014, 07:43

hi

i have this method MQL4

double lotsoptimized(){

double lot;

if(stoploss>0)lot=AccountBalance()*(risk/100)/(stoploss*pt/MarketInfo(Symbol(),MODE_TICKSIZE)*MarketInfo(Symbol(),MODE_TICKVALUE));

else lot=NormalizeDouble((AccountBalance()/1000)*minlot*risk,lotdigits);

//lot=AccountFreeMargin()/(100.0*(NormalizeDouble(MarketInfo(Symbol(),MODE_MARGINREQUIRED),4)+5.0)/risk)-0.05;

return(lot);

}

pt = Symbol.PointSize*10;

but in calgo lot just int

and i dont know how convert mql to calgo :)

please if you can convert this method

thank you

Replies

RootFX

11 Jul 2014, 09:55

( Updated at: 21 Dec 2023, 09:20 )

RE:

modarkat said:

Here you go

but it's work like this method 100% .?

double lotsoptimized(){

double lot;

if(stoploss>0)lot=AccountBalance()*(risk/100)/(stoploss*pt/MarketInfo(Symbol(),MODE_TICKSIZE)*MarketInfo(Symbol(),MODE_TICKVALUE));

else lot=NormalizeDouble((AccountBalance()/1000)*minlot*risk,lotdigits);

//lot=AccountFreeMargin()/(100.0*(NormalizeDouble(MarketInfo(Symbol(),MODE_MARGINREQUIRED),4)+5.0)/risk)-0.05;

return(lot);

}

@RootFX

RootFX

14 Jul 2014, 22:11

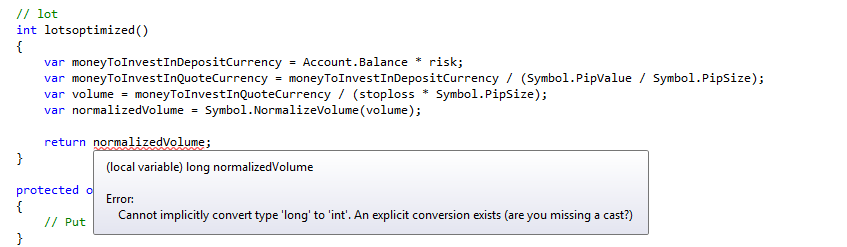

ok how edit this method

protected int GetVolume

{

get

{

var risk = (int)(RiskPct * Account.Balance / 100);

int volumeOnRisk = stoploss > 0 ? (int)(risk * Symbol.Ask / (Symbol.PipSize * stoploss)) : Volume;

double maxVolume = Account.Equity * Leverage * 100 / 101;

double vol = Math.Min(volumeOnRisk, maxVolume);

return (int)Math.Truncate(Math.Round(vol) / 10000) * 10000;

// round to 10K

}

}

you can set RiskPct like this 1% or 2 % ... etc

but i want calc in stoploss

@RootFX

modarkat

11 Jul 2014, 09:29

Here you go

/forum/cbot-support/2929

@modarkat