How to preset source in RSI indicator for a cBots, without manually setting?

How to preset source in RSI indicator for a cBots, without manually setting?

01 Jul 2020, 23:52

Hello,

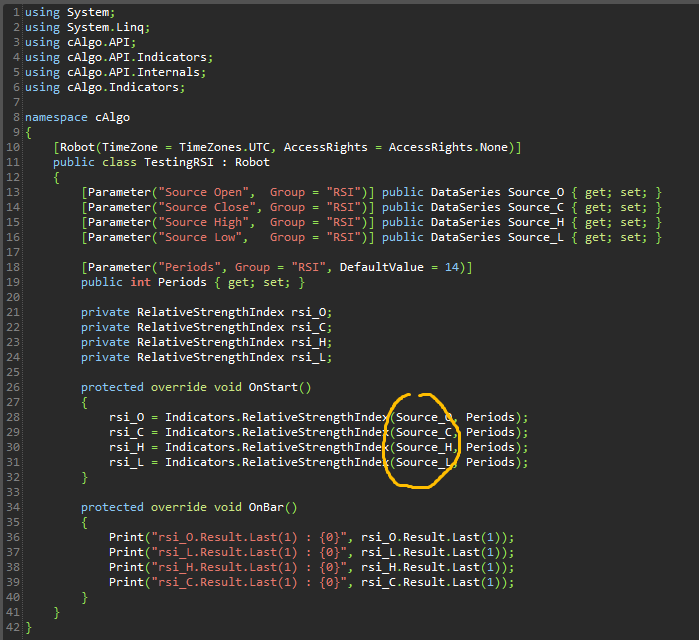

I have below testing code, it will return last 1st bar's RSI values based on Open/Close/High/Low price.

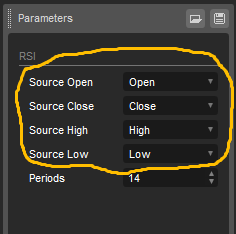

Now I want to preset sources for all the dataseries, but obviously I can't put string "Open" to replace Source_O, (in the highlighted area). What should I do to simplify the parameter setting area, to put all parameters preset in the coding stage rather than leave them for manually set?

Thank you again,

Lei

using System;

using System.Linq;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

using cAlgo.Indicators;

namespace cAlgo

{

[Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.None)]

public class TestingRSI : Robot

{

[Parameter("Source Open", Group = "RSI")] public DataSeries Source_O { get; set; }

[Parameter("Source Close", Group = "RSI")] public DataSeries Source_C { get; set; }

[Parameter("Source High", Group = "RSI")] public DataSeries Source_H { get; set; }

[Parameter("Source Low", Group = "RSI")] public DataSeries Source_L { get; set; }

[Parameter("Periods", Group = "RSI", DefaultValue = 14)]

public int Periods { get; set; }

private RelativeStrengthIndex rsi_O;

private RelativeStrengthIndex rsi_C;

private RelativeStrengthIndex rsi_H;

private RelativeStrengthIndex rsi_L;

protected override void OnStart()

{

rsi_O = Indicators.RelativeStrengthIndex(Source_O, Periods);

rsi_C = Indicators.RelativeStrengthIndex(Source_C, Periods);

rsi_H = Indicators.RelativeStrengthIndex(Source_H, Periods);

rsi_L = Indicators.RelativeStrengthIndex(Source_L, Periods);

}

protected override void OnBar()

{

Print("rsi_O.Result.Last(1) : {0}", rsi_O.Result.Last(1));

Print("rsi_L.Result.Last(1) : {0}", rsi_L.Result.Last(1));

Print("rsi_H.Result.Last(1) : {0}", rsi_H.Result.Last(1));

Print("rsi_C.Result.Last(1) : {0}", rsi_C.Result.Last(1));

}

}

}

Replies

Capt.Z-Partner

02 Jul 2020, 12:31

RE:

PanagiotisCharalampous said:

Hi Delphima,

Try the below

rsi_O = Indicators.RelativeStrengthIndex(Bars.OpenPrices, Periods); rsi_C = Indicators.RelativeStrengthIndex(Bars.ClosePrices, Periods); rsi_H = Indicators.RelativeStrengthIndex(Bars.HighPrices, Periods); rsi_L = Indicators.RelativeStrengthIndex(Bars.LowPrices, Periods);Best Regards,

Panagiotis

Hi Panagiotis,

This works well. Thank you very much.:)

Lei

@Capt.Z-Partner

PanagiotisCharalampous

02 Jul 2020, 08:50

Hi Delphima,

Try the below

Best Regards,

Panagiotis

Join us on Telegram

@PanagiotisCharalampous