Description

Exports chosen bars for Symbol at chosen at the chosen bar size from calgo to CSV file in Directory specified. Files can be imported by excel but do not open in when trying to update as excel takes an exclusive lock which will crash the process.

OK: Help Needed: When I run this in Backtest mode with 1 minute bars I get something that looks like valid volumes. When I run it with 10 tick bars I get the same volume in every bar. How do we get valid volume for the smaller duration bars.

Question: How do you convert (MarketSeries.TickVolume to actual Transaction volume for the Bar. I want Total number of units traded during the bar. I think transaction volume is a more meaningful input for momentum because a small transaction of a fractional unit doesn't mean as much as if a 100 million $ changed hands during the same change in price.

Recommended used is to use the Backtester to download as much historical data as possible in a back-test then switch over to activating the strategy live. It will auto-backfill the data between end of Backtest and live data but use the Backtest to get as much of the data as possible first as it's lastBar semantic is simplistic.

I have found that tickvolume is only accurate when the Backtest is using the "Tick Data from Server"

The system is smart enough to add new data from current Backtest to end of existing data and it will not overwrite or duplicate the older data but it is not smart enough to detect gaps if the user runs a Backtest covering a couple of months then skips a few months and runs a different Backtest.

When used live it will write a new bar whenever a bar has been completed for as long as the cbot is active. The files are opened in shared mode so a separate process can read new data from them as they arrive. I needed this because our AI prediction engine needs new data as it arrives and can not run inside of calgo. I will eventually write the reverse plumbing to allow predictions from the external engine to be picked up by calgo and executed as trades.

When used in back-tester will export the data in the time-frame specified by the backtest. I tested it back to Jan-1-2011 and all the data seemed to show up.

File name is derived from the symbol, bar duration and chosen moving average and looks like: exp-EURUSD-Minute-ma3-bars.b1.csv

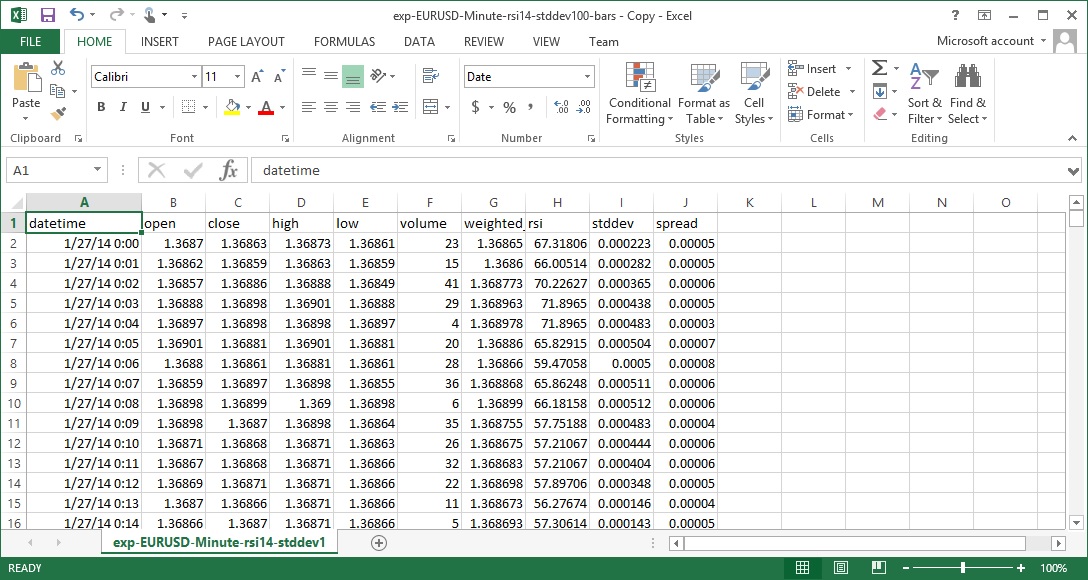

Data Looks as follows:

datetime,open,close,high,low,volume,weighted_val,rsi,stddev,spread

2014-01-27 00:00:00.000,1.368700,1.368630,1.368730,1.368610,23.000000,1.368650,67.318063,0.000223,0.000050

2014-01-27 00:01:00.000,1.368620,1.368590,1.368630,1.368590,15.000000,1.368600,66.005144,0.000282,0.000050

2014-01-27 00:02:00.000,1.368570,1.368860,1.368880,1.368490,41.000000,1.368773,70.226266,0.000365,0.000060

2014-01-27 00:03:00.000,1.368880,1.368980,1.369010,1.368880,29.000000,1.368963,71.896500,0.000438,0.000050

2014-01-27 00:04:00.000,1.368970,1.368980,1.368980,1.368970,4.000000,1.368978,71.896500,0.000483,0.000030

2014-01-27 00:05:00.000,1.369010,1.368810,1.369010,1.368810,20.000000,1.368860,65.829147,0.000504,0.000070

2014-01-27 00:06:00.000,1.368800,1.368610,1.368810,1.368610,28.000000,1.368660,59.470578,0.000500,0.000080

2014-01-27 00:07:00.000,1.368590,1.368970,1.368980,1.368550,36.000000,1.368868,65.862483,0.000511,0.000060

2014-01-27 00:08:00.000,1.368980,1.368990,1.369000,1.368980,6.000000,1.368990,66.181582,0.000512,0.000060

In Excel it looks like:

Note: To auto parse the dates when loading in excel change the code to replace T between dateTime with a space.

Enhanced Dec-21-2014: To only add bars newer than what are already present in the file but it is still missing the code to detect gaps and try to fill them in.

Enhanced Dec-212-2014 - To attempt to backfill bars between current bar and the last bar it finds in the file. This is needed because the the back tester in CAglo always runs a little behind the current data and would create a gap of some very critical missing current data. This process calculates how many are missing and attempts to backfile from current series. I have tested it over a weekend but not over longer periods of times.

Want to collaborate: www.linkedin.com/pub/joe-ellsworth/0/22/682/ or http://BayesAnalytic.com

No Promises, No Warranty.

// -------------------------------------------------------------------------------------------------

// DataExportBars

//

// This cBot is intended to download Bar level history to an external CSV File.

// Target file can not be open in excel or will fail to open export file. It can

// also be used to export live data when made Active during a trading session.

// Intended to allow shared read by other processes while this session is live which

// will allow external systems to analyze the data in near realtime.

//

// Export Historical

// To use set the Backtest Begin date and End Test Date to reflect desired date range.

// Set the time frame to Desired Bar Size

// Set the backtest Data to "Bars from Server"

// SElect the time frame desired for the extract.

// Then start the backtest.

//

// Important:

// To get accurate volume you must choose "Tick Data from Server (Accurate)"

// in the back test window. Then you can choose the desired bar resolution

// in the the Bar resolution in the instance settings.

//

//

// Tested with live data due the week of 12/10/2014 and it seems to work just fine.

//

// Can be used to download current Bars by runing as an active strategy.

// If you open the file in shared mode with a readline() pending it will

// deliver new bars as they become available but will always be 1 bar behind

// because it has to wait until the bar is complete. If you need data

// faster use a shorter bar or consider DataExportTicks

//

// When using to read data in other processes suggest using fast memory

// RamDrive or fast SSD. Otherwise may need to use NamedPipe. Our other

// technology running in a separate process did not support windows

// named pipes so just using a fast SSD and seems to work. Will eventually

// need to add function which detects when there is a new hour and open

// new file so we do grow the files too large.

//

// Note: If you load the CSV files in excell and the save again it will mess

// up the dateTime unless you set the Excel dat format for the column.

// to: Date -> 3/14/12 13:30

//

// Want to collaborate: www.linkedin.com/pub/joe-ellsworth/0/22/682/ or

// http://bayesanalytic.com

//

// No Promises, No Warranty. Terms of use MIT http://opensource.org/licenses/MIT

//

// -------------------------------------------------------------------------------------------------

using System;

using System.IO;

using System.Linq;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

using cAlgo.Indicators;

namespace cAlgo

{

[Robot(TimeZone = TimeZones.UTC, AccessRights = AccessRights.FileSystem)]

public class DataExportBars : Robot

{

[Parameter("MA Source")]

public DataSeries Source { get; set; }

[Parameter("RSI Period", DefaultValue = 14)]

public int RSIPeriod { get; set; }

[Parameter("StdDev Period", DefaultValue = 100)]

public int StdDevPeriod { get; set; }

[Parameter("Data Dir", DefaultValue = "c:\\download\\calgo")]

public string DataDir { get; set; }

const string dateFormat = "yyyy-MM-dd HH:mm:ss.fff";

private RelativeStrengthIndex rsi;

private StandardDeviation stdDev;

private string fiName;

private System.IO.FileStream fstream;

private System.IO.StreamWriter fwriter;

private string csvhead = "datetime,open,close,high,low,volume,weighted_val,rsi,stddev,spread\n";

private string maxDate = "";

private bool isFirstBar = true;

// max date processed so far.

// We do not want to re-write dates that are already in the file so

// we scan to the last line in the file and record that date times.

// when running in history mode we simply skip any bars that occur

// before last date.

protected string get_most_recent_date(string fiName)

{

Print("start get_most_recent_date");

string maxDateRead = "";

if (System.IO.File.Exists(fiName) == false)

{

return "";

}

using (var readStream = File.Open(fiName, FileMode.Open, FileAccess.Read, FileShare.Read))

{

// setup to append to end of file

Print("grd File is Open");

readStream.Seek(readStream.Length - 5000, SeekOrigin.Begin);

// We know that our average bar line is under 120 bytes so skipping back

// by 2K bytes gives us plenty of margin to read the last line without

// readin the entire file.

var freader = new System.IO.StreamReader(readStream, System.Text.Encoding.UTF8);

Print("grd Got freader for " + fiName);

while (true)

{

string fline = freader.ReadLine();

if (fline == null)

{

break;

}

fline = fline.Trim();

string[] tflds = fline.Split(',');

string currDate = tflds[0].Trim();

if (currDate.Length > 20)

{

// minimum DateTime is 20 bytes so must not be

// a datetime if it is less. Should probably have

// a more sophisticated check.

if (currDate.CompareTo(maxDateRead) > 0)

{

maxDateRead = currDate;

}

}

}

// while

readStream.Close();

// using statement above will close stream anyway

Print("grd returning " + maxDateRead);

return maxDateRead;

}

// using

}

// func()

protected override void OnStart()

{

// demonstrate using indicators easier to compute in pre-build cAlgo

// code than to compute in the external system.

//rsiBase = Indicators.RelativeStrengthIndex(DataSeries, RSIPeriod);

rsi = Indicators.RelativeStrengthIndex(Source, RSIPeriod);

stdDev = Indicators.StandardDeviation(Source, RSIPeriod, MovingAverageType.Simple);

var ticktype = MarketSeries.TimeFrame.ToString();

fiName = DataDir + "\\" + "exp-" + Symbol.Code + "-" + ticktype + "-rsi" + RSIPeriod + "-stddev" + StdDevPeriod + "-bars.csv";

Print("fiName=" + fiName);

if (System.IO.Directory.Exists(DataDir) == false)

{

System.IO.Directory.CreateDirectory(DataDir);

}

if (System.IO.File.Exists(fiName) == false)

{

// generate new file with CSV header only if

// one does not already exist.

System.IO.File.WriteAllText(fiName, csvhead);

}

else

{

maxDate = get_most_recent_date(fiName);

}

Print("maxDate=" + maxDate);

// had to open file this way to prevent .net from locking it and preventing

// access by other processes when using to download live ticks.

fstream = File.Open(fiName, FileMode.Open, FileAccess.Write, FileShare.ReadWrite);

// setup to append to end of file

Print("File is Open");

fstream.Seek(0, SeekOrigin.End);

// write stream has to be created after seek due to .net wierdness

// creating with 0 prevents buffering since we want tick data

// to be available to consumers right away.

fwriter = new System.IO.StreamWriter(fstream, System.Text.Encoding.UTF8, 1);

// QUESTION: How to tell when in Backtest mode so we

// can create the stream with a large buffer and turn off

// auto flush to improve IO performance.

Print("Fwriter is created");

fwriter.AutoFlush = true;

// with autoflush true will autocleanup

// since we can not close since we may run forever

Print("done onStart()");

}

protected void save_bar(int last_minus)

{

var sa = new System.Collections.Generic.List<string>();

var barTime = MarketSeries.OpenTime.Last(last_minus);

var timestr = barTime.ToString(dateFormat);

if (timestr.CompareTo(maxDate) > 0)

{

// only save if our date is newer than what

// we already have.

maxDate = timestr;

// had to use last(1) because the onBar is called

// when the bar is first formed. Otherwise it would

// return incomplete bars when running live.

sa.Add(timestr);

sa.Add(MarketSeries.Open.Last(last_minus).ToString("F6"));

sa.Add(MarketSeries.Close.Last(last_minus).ToString("F6"));

sa.Add(MarketSeries.High.Last(last_minus).ToString("F6"));

sa.Add(MarketSeries.Low.Last(last_minus).ToString("F6"));

// QUESTION: HOw to Get the actual Buy / sell volume

// Rather than number of Ticks. Both may be useful

// But the transaction volume is a critical component

// for many indicators.

sa.Add(MarketSeries.TickVolume.Last(last_minus).ToString("F6"));

sa.Add(MarketSeries.WeightedClose.Last(last_minus).ToString("F6"));

sa.Add(rsi.Result.Last(last_minus).ToString("F6"));

sa.Add(stdDev.Result.Last(last_minus).ToString("F6"));

sa.Add(Symbol.Spread.ToString("F6"));

var sout = string.Join(",", sa);

fwriter.WriteLine(sout);

}

}

// Try to export recent bars to fill in the gap between

// backtest and live running data. EG: Backtest stoped on

// 12/19 but we have new bars that have occured on 12/21 when

// starting live. Not including the bars from earlier today

// will skew most recent statistics.

protected void process_earlier_bars()

{

Print("process_earlier_bars last_date_in_file=" + maxDate);

if (maxDate == "")

{

// brand new file so do not need to worry about gaps

Print("maxDate is empty in process_earlier_bars");

}

else

{

Print("checking earlier bars last Date in File=" + maxDate);

var lastBarTime = MarketSeries.OpenTime.Last(1);

var priorBarTime = MarketSeries.OpenTime.Last(2);

var lastSavedDate = System.DateTime.ParseExact(maxDate, dateFormat, System.Globalization.CultureInfo.InvariantCulture);

double secondsPerBar = (lastBarTime - priorBarTime).TotalSeconds;

double missingseconds = (lastBarTime - lastSavedDate).TotalSeconds;

int missingbars = (int)(missingseconds / secondsPerBar) + 1;

Print("secondsPerBar=" + secondsPerBar + " missingseconds= " + missingseconds + " missingbars=" + missingbars);

var fillBarTime = MarketSeries.OpenTime.Last(missingbars);

Print("fillBarTime=" + fillBarTime.ToUniversalTime());

for (int last_minus = missingbars; last_minus > 1; last_minus--)

{

save_bar(last_minus);

}

}

}

// Event handler called by CAlgo for every bar that occurs

protected override void OnBar()

{

if (isFirstBar)

{

process_earlier_bars();

isFirstBar = false;

}

save_bar(1);

}

protected override void OnStop()

{

Print("OnStop()");

fwriter.Close();

fstream.Close();

// Put your deinitialization logic here

}

}

}

joeatbayes

Joined on 06.12.2014

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: csvbar.algo

- Rating: 5

- Installs: 4137

- Modified: 13/10/2021 09:54

Comments

Dumpsbuddy provides you the latest, updated, and authentic C_S4CDK_2022 exam dumps. We know that there are multiple sources for the preparation of SAP Certified Development Associate C_S4CDK_2022 exam but clients don’t know for whom they should go? Well, a client can check the C_S4CDK_2022 dumps pdf questions by taking a trial of a free demo so that he can get an idea about the questions of the SAP C_S4CDK_2022 exam.

Works great, Thanks.

One question: Can we change the order of CSV columns to OHLC without too much bother?

The files which are generated with this cBot are not compatible with cAlgo. There is an error message popping up.

What's the purpose of publishing a cBot if it does not do what it is supposed to do?

The 200-901 crack dumps, also known as the DevNet Associate exam, is a certification offered by Cisco for individuals interested in pursuing a career in software development, DevOps, or network automation. This exam focuses on testing a candidate's understanding of software development and design principles, APIs, networking fundamentals, and automation tools.