Warning! This section will be deprecated on February 1st 2025. Please move all your Indicators to the cTrader Store catalogue.

Description

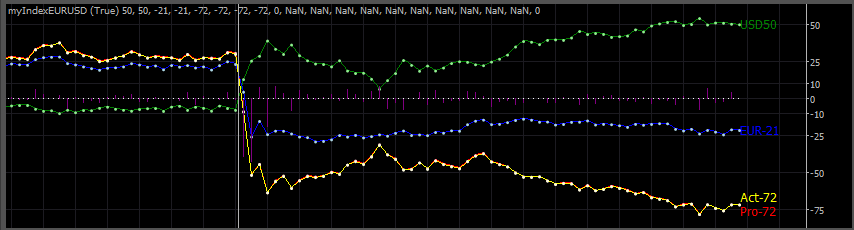

Determines the daily increase or decrease in the value of the Euro and Dollar.The actual and projected value of the pair is also plotted.

using System;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo.Indicators

{

[Indicator(IsOverlay = false, AutoRescale = true, ScalePrecision = 0, TimeZone = TimeZones.UTC)]

[Levels(-75, 75, -50, 50, -25, 25, 10, -10, 0, 100,

-100)]

public class myIndexEURUSD : Indicator

{

[Parameter(DefaultValue = false)]

public bool HideYeilds { get; set; }

[Output("USD Index", Color = Colors.Green)]

public IndicatorDataSeries USDIDX { get; set; }

[Output("USD Points", Color = Colors.LightGreen, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries USDIDXPoints { get; set; }

[Output("EUR Index", Color = Colors.Blue)]

public IndicatorDataSeries EURIDX { get; set; }

[Output("EUR Points", Color = Colors.LightBlue, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries EURIDXPoints { get; set; }

[Output("ProjYld", Color = Colors.Red)]

public IndicatorDataSeries ProjYld { get; set; }

[Output("ProjYld Points", Color = Colors.Pink, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries ProjYldPoints { get; set; }

[Output("ActYld", Color = Colors.Yellow)]

public IndicatorDataSeries ActYld { get; set; }

[Output("ActYld Points", Color = Colors.LightYellow, Thickness = 2, PlotType = PlotType.Points)]

public IndicatorDataSeries ActYldPoints { get; set; }

[Output("Delta", PlotType = PlotType.Histogram, Color = Colors.Purple)]

public IndicatorDataSeries Delta { get; set; }

//[Output("EURUSD", Color = Colors.Blue)]

//public IndicatorDataSeries Yeild1 { get; set; }

[Output("USDJPY", Color = Colors.Red)]

public IndicatorDataSeries YldUSDJPY { get; set; }

[Output("GBPUSD", Color = Colors.Yellow)]

public IndicatorDataSeries YldGBPUSD { get; set; }

[Output("AUDUSD", Color = Colors.Purple)]

public IndicatorDataSeries YldAUDUSD { get; set; }

[Output("USDCHF", Color = Colors.OrangeRed)]

public IndicatorDataSeries YldUSDCHF { get; set; }

[Output("EURJPY", Color = Colors.Pink)]

public IndicatorDataSeries YldEURJPY { get; set; }

[Output("EURGBP", Color = Colors.LightYellow)]

public IndicatorDataSeries YldEURGBP { get; set; }

[Output("EURAUD", Color = Colors.Orchid)]

public IndicatorDataSeries YldEURAUD { get; set; }

[Output("EURCHF", Color = Colors.Orange)]

public IndicatorDataSeries YldEURCHF { get; set; }

[Output("BuySignal", Color = Colors.Blue, Thickness = 5, PlotType = PlotType.Points)]

public IndicatorDataSeries BuySignal { get; set; }

[Output("SellSignal", Color = Colors.Red, Thickness = 5, PlotType = PlotType.Points)]

public IndicatorDataSeries SellSignal { get; set; }

[Output("Center", LineStyle = LineStyle.DotsRare, Color = Colors.White)]

public IndicatorDataSeries CenterLine { get; set; }

private MarketSeries msUSDJPY, msGBPUSD, msAUDUSD, msUSDCHF, msEURJPY, msEURGBP, msEURAUD, msEURCHF;

protected override void Initialize()

{

string IndicatorName = GetType().ToString().Substring(GetType().ToString().LastIndexOf('.') + 1);

// returns ClassName

Print("Indicator: " + IndicatorName);

Print("IndicatorTimeZone: {0} Offset: {1} DST: {2}", TimeZone, TimeZone.BaseUtcOffset, TimeZone.SupportsDaylightSavingTime);

msUSDJPY = MarketData.GetSeries("USDJPY", TimeFrame);

msGBPUSD = MarketData.GetSeries("GBPUSD", TimeFrame);

msAUDUSD = MarketData.GetSeries("AUDUSD", TimeFrame);

msUSDCHF = MarketData.GetSeries("USDCHF", TimeFrame);

msEURJPY = MarketData.GetSeries("EURJPY", TimeFrame);

msEURGBP = MarketData.GetSeries("EURGBP", TimeFrame);

msEURAUD = MarketData.GetSeries("EURAUD", TimeFrame);

msEURCHF = MarketData.GetSeries("EURCHF", TimeFrame);

}

public override void Calculate(int index)

{

if (index < 1)

return;

int idxEURUSD = index;

var idxUSDJPY = msUSDJPY.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxGBPUSD = msGBPUSD.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxAUDUSD = msAUDUSD.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxUSDCHF = msUSDCHF.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURJPY = msEURJPY.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURGBP = msEURGBP.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURAUD = msEURAUD.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

var idxEURCHF = msEURCHF.OpenTime.GetIndexByTime(MarketSeries.OpenTime[idxEURUSD]);

int idxEURUSDn = DailyPeriodAdjustment(MarketSeries, idxEURUSD);

var idxUSDJPYn = DailyPeriodAdjustment(msUSDJPY, idxUSDJPY);

var idxGBPUSDn = DailyPeriodAdjustment(msGBPUSD, idxGBPUSD);

var idxAUDUSDn = DailyPeriodAdjustment(msAUDUSD, idxAUDUSD);

var idxUSDCHFn = DailyPeriodAdjustment(msUSDCHF, idxUSDCHF);

var idxEURJPYn = DailyPeriodAdjustment(msEURJPY, idxEURJPY);

var idxEURGBPn = DailyPeriodAdjustment(msEURGBP, idxEURGBP);

var idxEURAUDn = DailyPeriodAdjustment(msEURAUD, idxEURAUD);

var idxEURCHFn = DailyPeriodAdjustment(msEURCHF, idxEURCHF);

double yldEURUSD = ((MarketSeries.Close[idxEURUSD] - MarketSeries.Close[idxEURUSD - idxEURUSDn]) / MarketSeries.Close[idxEURUSD - idxEURUSDn]) * 10000;

double yldUSDJPY = ((msUSDJPY.Close[idxUSDJPY] - msUSDJPY.Close[idxUSDJPY - idxUSDJPYn]) / msUSDJPY.Close[idxUSDJPY - idxUSDJPYn]) * 10000;

double yldGBPUSD = -((msGBPUSD.Close[idxGBPUSD] - msGBPUSD.Close[idxGBPUSD - idxGBPUSDn]) / msGBPUSD.Close[idxGBPUSD - idxGBPUSDn]) * 10000;

double yldAUDUSD = -((msAUDUSD.Close[idxAUDUSD] - msAUDUSD.Close[idxAUDUSD - idxAUDUSDn]) / msAUDUSD.Close[idxAUDUSD - idxAUDUSDn]) * 10000;

double yldUSDCHF = ((msUSDCHF.Close[idxUSDCHF] - msUSDCHF.Close[idxUSDCHF - idxUSDCHFn]) / msUSDCHF.Close[idxUSDCHF - idxUSDCHFn]) * 10000;

double yldEURJPY = ((msEURJPY.Close[idxEURJPY] - msEURJPY.Close[idxEURJPY - idxEURJPYn]) / msEURJPY.Close[idxEURJPY - idxEURJPYn]) * 10000;

double yldEURGBP = ((msEURGBP.Close[idxEURGBP] - msEURGBP.Close[idxEURGBP - idxEURGBPn]) / msEURGBP.Close[idxEURGBP - idxEURGBPn]) * 10000;

double yldEURAUD = ((msEURAUD.Close[idxEURAUD] - msEURAUD.Close[idxEURAUD - idxEURAUDn]) / msEURAUD.Close[idxEURAUD - idxEURAUDn]) * 10000;

double yldEURCHF = ((msEURCHF.Close[idxEURCHF] - msEURCHF.Close[idxEURCHF - idxEURCHFn]) / msEURCHF.Close[idxEURCHF - idxEURCHFn]) * 10000;

if (!HideYeilds)

{

YldUSDJPY[index] = yldUSDJPY;

YldGBPUSD[index] = yldGBPUSD;

YldAUDUSD[index] = yldAUDUSD;

YldUSDCHF[index] = yldUSDCHF;

YldEURJPY[index] = yldEURJPY;

YldEURGBP[index] = yldEURGBP;

YldEURAUD[index] = yldEURAUD;

YldEURCHF[index] = yldEURCHF;

}

double usdidx0 = (yldUSDJPY + yldGBPUSD + yldAUDUSD + yldUSDCHF) / 4;

double euridx0 = (yldEURJPY + yldEURGBP + yldEURAUD + yldEURCHF) / 4;

double usdidx1 = USDIDX[index - 1];

double euridx1 = EURIDX[index - 1];

double USDdelta = usdidx0 - usdidx1;

double EURdelta = euridx0 - euridx1;

USDIDX[index] = usdidx0;

USDIDXPoints[index] = usdidx0;

EURIDX[index] = euridx0;

EURIDXPoints[index] = euridx0;

ActYld[index] = yldEURUSD;

ActYldPoints[index] = yldEURUSD;

ProjYld[index] = euridx0 - usdidx0;

ProjYldPoints[index] = euridx0 - usdidx0;

Delta[index] = EURdelta - USDdelta;

//if(USDdelta>0 && EURdelta<0 && -EURdelta>=USDdelta)SellSignal[index]=0;

//if(delta1<0 && delta2>0)BuySignal[index]=0;

CenterLine[index] = 0;

string USDTxt = string.Format("USD{0}", Math.Round(USDIDX[index], 0));

string EURTxt = string.Format("EUR{0}", Math.Round(EURIDX[index], 0));

string ACTTxt = string.Format("Act{0}", Math.Round(ActYld[index], 0));

string PROJTxt = string.Format("Pro{0}", Math.Round(ProjYld[index], 0));

ChartObjects.DrawText("USDlabel", USDTxt, index, USDIDX[index], VerticalAlignment.Center, HorizontalAlignment.Right, Colors.Green);

ChartObjects.DrawText("EURlabel", EURTxt, index, EURIDX[index], VerticalAlignment.Center, HorizontalAlignment.Right, Colors.Blue);

ChartObjects.DrawText("ACTlabel", ACTTxt, index, ActYld[index], VerticalAlignment.Top, HorizontalAlignment.Right, Colors.Yellow);

ChartObjects.DrawText("PROJlabel", PROJTxt, index, ProjYld[index], VerticalAlignment.Bottom, HorizontalAlignment.Right, Colors.Red);

}

private int DailyPeriodAdjustment(MarketSeries ms, int index)

{

if (index < 1) return 0;

int periods = 1;

DateTime CurrentDate = ms.OpenTime[index].AddHours(2);

DateTime PreviousDate = ms.OpenTime[index - periods].AddHours(2);

int DateDifference = (int)(CurrentDate.Date - PreviousDate.Date).TotalDays;

while (CurrentDate.DayOfWeek == PreviousDate.DayOfWeek || PreviousDate.DayOfWeek == DayOfWeek.Sunday || CurrentDate.DayOfWeek == DayOfWeek.Saturday)

{

periods++;

if (index < periods)

return periods - 1;

PreviousDate = ms.OpenTime[index - periods].AddHours(2);

DateDifference = (int)(CurrentDate.Date - PreviousDate.Date).TotalDays;

}

return periods - 1;

}

}

}

lec0456

Joined on 14.11.2012

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: myIndexEURUSD.algo

- Rating: 5

- Installs: 4565

- Modified: 13/10/2021 09:54

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

Thank you, this is a really nice strength indicator for finding you trades :)