Warning! This section will be deprecated on February 1st 2025. Please move all your Indicators to the cTrader Store catalogue.

Description

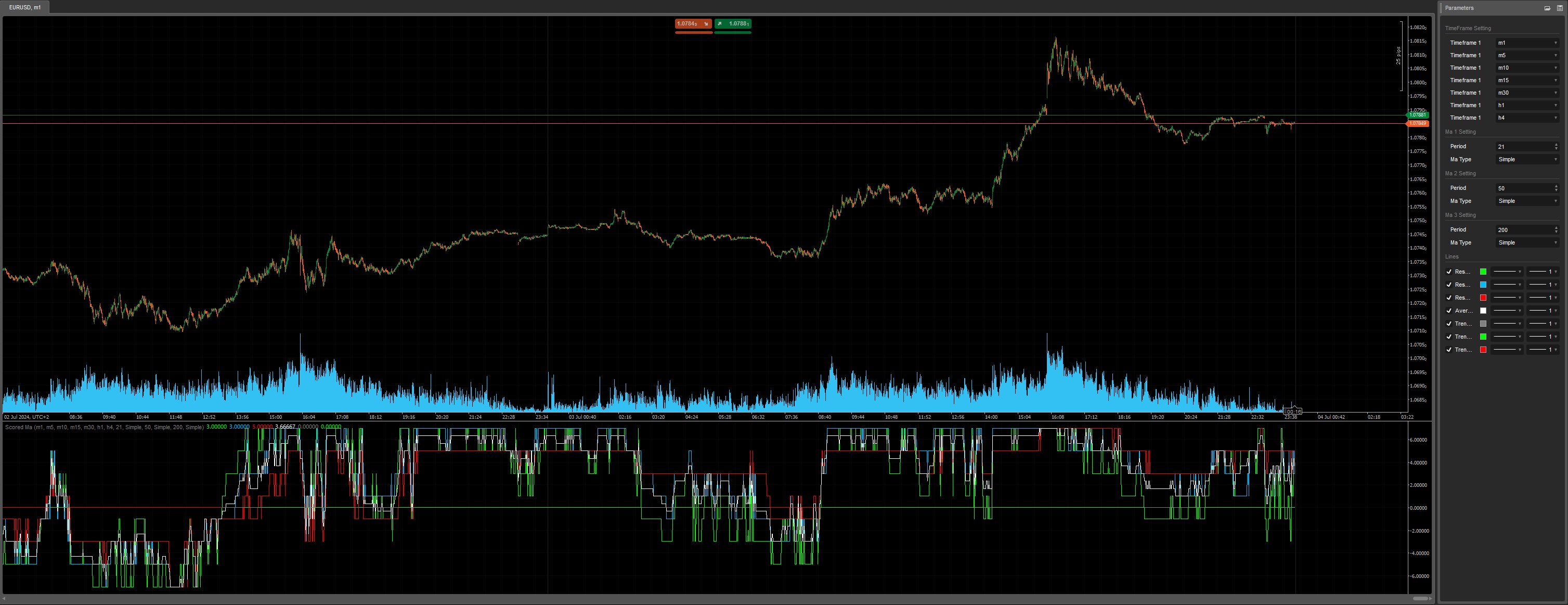

This indicator uses the scoring strategy to define a signal. If a bar is above a moving average (MA), the score is +1, and if a bar is below a moving average (MA), the score is -1. This analysis is applied to 3 different moving averages and 7 different timeframes.

Output:

- 3 different results, each result corresponding to a specific moving average across 7 different timeframes.

- 1 average of the 3 different results.

- 1 trend indicator that determines if all results are above or below 0.

Enjoy for Free =)

Previous account here : https://ctrader.com/users/profile/70920

Contact telegram : https://t.me/nimi012

using System;

using System.Collections.Generic;

using System.Linq;

using System.Text;

using cAlgo.API;

using cAlgo.API.Collections;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

namespace cAlgo

{

[Indicator(AccessRights = AccessRights.None)]

public class ScoredMa : Indicator

{

[Parameter("Timeframe 1", DefaultValue = "Minute", Group = "TimeFrame Setting")]

public TimeFrame Timeframe1 { get; set; }

[Parameter("Timeframe 1", DefaultValue = "Minute5", Group = "TimeFrame Setting")]

public TimeFrame Timeframe2 { get; set; }

[Parameter("Timeframe 1", DefaultValue = "Minute10", Group = "TimeFrame Setting")]

public TimeFrame Timeframe3 { get; set; }

[Parameter("Timeframe 1", DefaultValue = "Minute15", Group = "TimeFrame Setting")]

public TimeFrame Timeframe4 { get; set; }

[Parameter("Timeframe 1", DefaultValue = "Minute30", Group = "TimeFrame Setting")]

public TimeFrame Timeframe5 { get; set; }

[Parameter("Timeframe 1", DefaultValue = "Hour", Group = "TimeFrame Setting")]

public TimeFrame Timeframe6 { get; set; }

[Parameter("Timeframe 1", DefaultValue = "Hour4", Group = "TimeFrame Setting")]

public TimeFrame Timeframe7 { get; set; }

[Parameter("Period", DefaultValue = 21, Group = "Ma 1 Setting")]

public int PeriodMa1 { get; set; }

[Parameter("Ma Type", DefaultValue = 21, Group = "Ma 1 Setting")]

public MovingAverageType MaTypeMa1 { get; set; }

[Parameter("Period ", DefaultValue = 50, Group = "Ma 2 Setting")]

public int PeriodMa2 { get; set; }

[Parameter("Ma Type", DefaultValue = 21, Group = "Ma 2 Setting")]

public MovingAverageType MaTypeMa2 { get; set; }

[Parameter("Period", DefaultValue = 200, Group = "Ma 3 Setting")]

public int PeriodMa3 { get; set; }

[Parameter("Ma Type", DefaultValue = 21, Group = "Ma 3 Setting")]

public MovingAverageType MaTypeMa3 { get; set; }

[Output("Result Ma 1", LineColor = "Lime")]

public IndicatorDataSeries ResultMa1 { get; set; }

[Output("Result Ma 2", LineColor = "DeepSkyBlue")]

public IndicatorDataSeries ResultMa2 { get; set; }

[Output("Result Ma 3", LineColor = "Red")]

public IndicatorDataSeries ResultMa3 { get; set; }

[Output("Average", LineColor = "White")]

public IndicatorDataSeries Average { get; set; }

[Output("Trend Mid", PlotType = PlotType.DiscontinuousLine, LineColor = "Gray")]

public IndicatorDataSeries TrendMid { get; set; }

[Output("Trend Up", PlotType = PlotType.DiscontinuousLine, LineColor = "Lime")]

public IndicatorDataSeries TrendUp { get; set; }

[Output("Trend Down", PlotType = PlotType.DiscontinuousLine, LineColor = "Red")]

public IndicatorDataSeries TrendDown { get; set; }

private MovingAverage[] ema1, ema2, ema3;

private Bars[] barsTF;

private int[] indexTF;

private IndicatorDataSeries[] mas1, mas2, mas3;

protected override void Initialize()

{

ema1 = new MovingAverage[7];

ema2 = new MovingAverage[7];

ema3 = new MovingAverage[7];

barsTF = new Bars[7];

barsTF[0] = MarketData.GetBars(Timeframe1);

barsTF[1] = MarketData.GetBars(Timeframe2);

barsTF[2] = MarketData.GetBars(Timeframe3);

barsTF[3] = MarketData.GetBars(Timeframe4);

barsTF[4] = MarketData.GetBars(Timeframe5);

barsTF[5] = MarketData.GetBars(Timeframe6);

barsTF[6] = MarketData.GetBars(Timeframe7);

indexTF = new int[7];

mas1 = new IndicatorDataSeries[7];

mas2 = new IndicatorDataSeries[7];

mas3 = new IndicatorDataSeries[7];

for (int i = 0; i < 7; i++)

{

if (!IsBacktesting)

{

while (barsTF[i].OpenTimes[0] > Bars.OpenTimes[0])

barsTF[i].LoadMoreHistory();

}

ema1[i] = Indicators.MovingAverage(barsTF[i].ClosePrices, PeriodMa1, MaTypeMa1);

ema2[i] = Indicators.MovingAverage(barsTF[i].ClosePrices, PeriodMa2, MaTypeMa2);

ema3[i] = Indicators.MovingAverage(barsTF[i].ClosePrices, PeriodMa3, MaTypeMa3);

mas1[i] = CreateDataSeries();

mas2[i] = CreateDataSeries();

mas3[i] = CreateDataSeries();

}

}

public override void Calculate(int index)

{

double count1 = 0;

double count2 = 0;

double count3 = 0;

for (int i = 0; i < 7; i++)

{

indexTF[i] = barsTF[i].OpenTimes.GetIndexByTime(Bars.OpenTimes.Last(0));

mas1[i][index] = Bars.ClosePrices.Last(0) > ema1[i].Result[indexTF[i]] ? 1

: Bars.ClosePrices.Last(0) < ema1[i].Result[indexTF[i]] ? -1 : 0;

mas2[i][index] = Bars.ClosePrices.Last(0) > ema2[i].Result[indexTF[i]] ? 1

: Bars.ClosePrices.Last(0) < ema2[i].Result[indexTF[i]] ? -1 : 0;

mas3[i][index] = Bars.ClosePrices.Last(0) > ema3[i].Result[indexTF[i]] ? 1

: Bars.ClosePrices.Last(0) < ema3[i].Result[indexTF[i]] ? -1 : 0;

count1 += mas1[i][index];

count2 += mas2[i][index];

count3 += mas3[i][index];

}

ResultMa1[index] = count1;

ResultMa2[index] = count2;

ResultMa3[index] = count3;

Average[index] = (ResultMa1[index] + ResultMa2[index] + ResultMa3[index]) / 3;

TrendMid[index] = 0;

TrendUp[index] = ResultMa1[index] > 0 && ResultMa2[index] > 0 && ResultMa3[index] > 0 ? 0 : double.NaN;

TrendDown[index] = ResultMa1[index] < 0 && ResultMa2[index] < 0 && ResultMa3[index] < 0 ? 0 : double.NaN;

}

}

}

YE

YesOrNot2

Joined on 17.05.2024

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: Scored Ma.algo

- Rating: 5

- Installs: 508

- Modified: 03/07/2024 22:02

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

No comments found.