Warning! This section will be deprecated on February 1st 2025. Please move all your Indicators to the cTrader Store catalogue.

An update for this algorithm is currently pending moderation. Please revisit this page shortly to access the algorithm's latest version.

Description

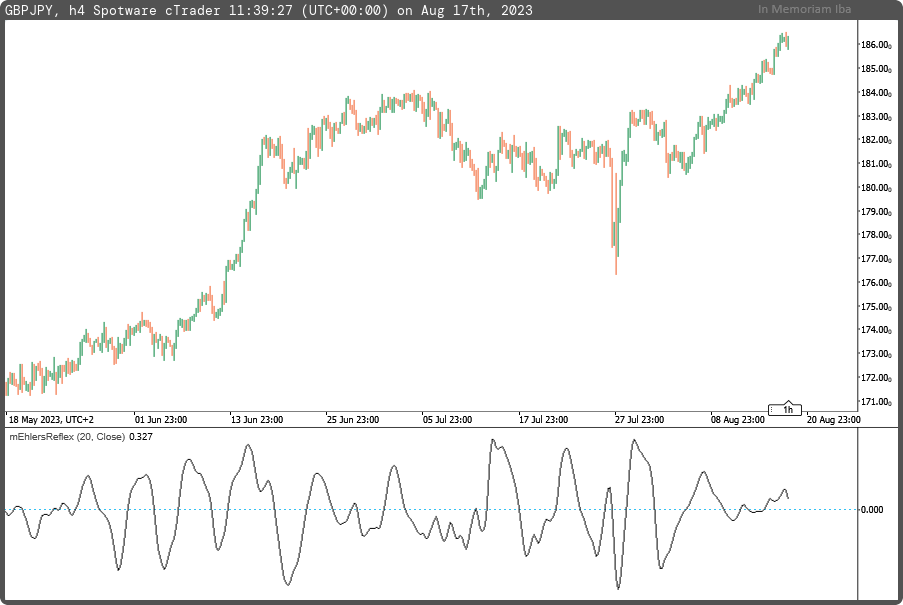

John Ehlers indicator "Reflex: A New Zero-Lag Indicator" - February 2020.

In "Reflex: A New Zero-Lag Indicator," author John Ehlers introduces a groundbreaking averaging indicator meticulously crafted to minimize lag. This indicator represents a significant leap forward in reducing time delays inherent in traditional calculations. According to Ehlers, this innovative indicator holds the capability to produce signals with greater timeliness compared to conventional lagging computations.

mfejza

Joined on 25.01.2022

- Distribution: Free

- Language: C#

- Trading platform: cTrader Automate

- File name: mEhlersReflex.algo

- Rating: 0

- Installs: 515

- Modified: 17/08/2023 11:43

Note that publishing copyrighted material is strictly prohibited. If you believe there is copyrighted material in this section, please use the Copyright Infringement Notification form to submit a claim.

Comments

Log in to add a comment.

MF

mfejza

·

1 year ago