Description

qqq

The author decided to hide the source code.

fxblackdragon

Joined on 02.07.2024

- Distribution: Paid

- Language: C#

- Trading platform: cTrader Automate

- File name: Catch trend 3MA_withSourceCode.algo

- Rating: 3.33

- Installs: 0

- Modified: 18/01/2025 08:44

Comments

يبدي جيداً لي عودة لاختبارة هل لك ان تخبرني كم تكلفتة

You should only backtest tick data because other data cannot be used as a reference.

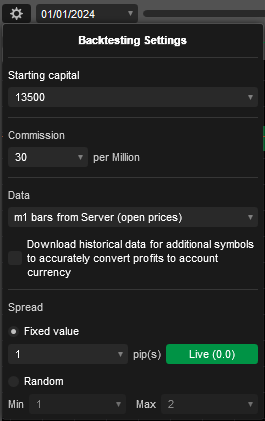

yes, as jay mentions, no matter what timeframe you are targeting, you should use tick data as your historical data source as this represents with 99% accuracy, the data that is occurring in real-time. using m1 as the data source is next to useless and will almost certainly skew your results to produce a very favourable chart which can't be replicated in live. You should adjust this in the [Backtesting Settings] tab as such:

Rather than using:

Once you do this, your backtesting/optimisation should reflect the expected outcomes on LIVE.

Hope this helps.

It should be backtested using tick data only

Backtesting Result last 10 years screenshot is uploaded.

Do you have a trial version so I can backtest it over the last 10 years?

Tick data backtesting result